Manufacturing in the Heartland

History plays a large role in determining the economic base of a region, and it certainly explains why manufacturing is the largest industry by output in the Heartland (manufacturing alone generates one-fifth of regional gross domestic product), the 2nd largest employer in the region (13 percent of total private employment), and the 2nd most concentrated industry in the region (employment is 1.3 times more concentrated in the Heartland than the U.S.). Mining is the most concentrated industry, having 1.65 times more employment in the region than the U.S., which reflects the rich mineral resources that underlie the region.1 Mining products are heavy and difficult to transport, so it was common during the early stages of the industrial revolution (prior to transcontinental railroads, for example) for manufacturing to locate near the raw materials needed to minimize transportation costs. As the mills grew in both output and employment, they became entrenched in these communities so that efficiencies from skilled labor pools, specialized inputs, and other factors associated with industry concentration offset any savings from falling transportation costs over the years.

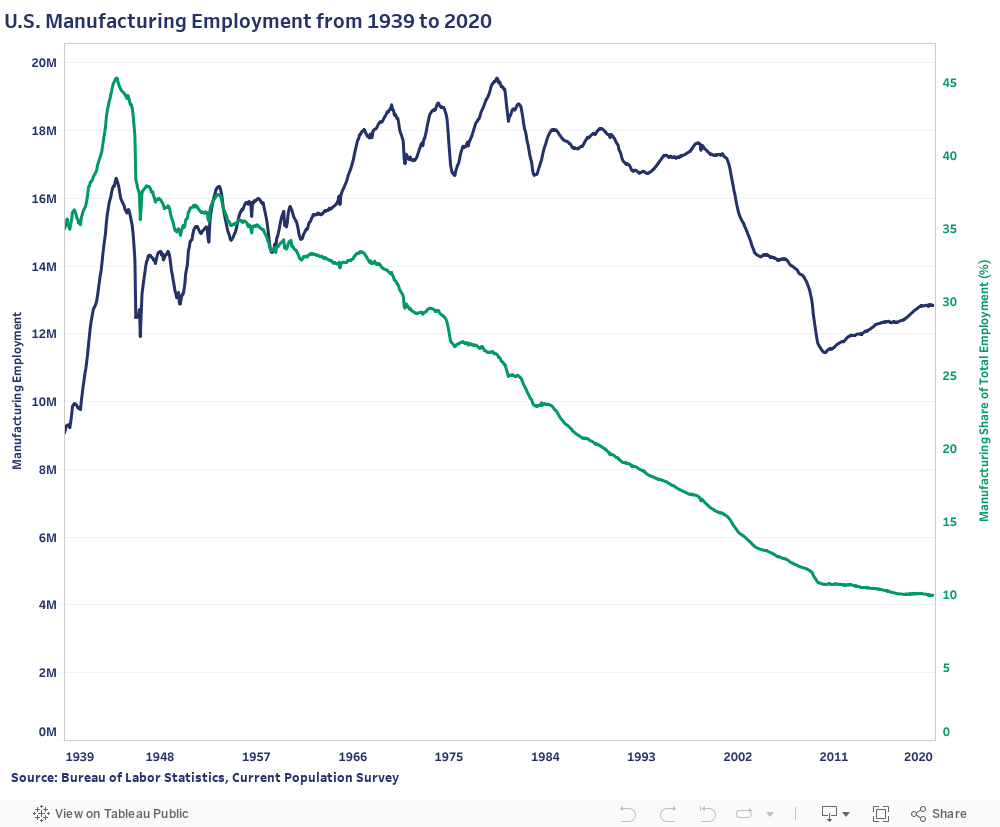

Despite what you might have read, manufacturing employment has not vanished from the U.S. economy. As the chart below illustrates, manufacturing employment is higher now than in 1939 (when the data series begins), though admittedly it’s not as high as in 1980 when manufacturing employment peaked. What has caused concern is the dramatic decline in the share of manufacturing employment – which has steadily declined since its peak in 1944. As the U.S. economy has grown over the 20th and 21st centuries, manufacturing has declined in importance from 35 percent of total employment in 1939 to 10 percent in 2019.

The decline in manufacturing accelerated in the 1970s, as automation was introduced into manufacturing, which increased productivity and output. While automation can displace workers from the tasks it performs, it also created a need for more employees to manage the increased volume of output generated, as well as to program and maintain the robots and equipment.2 (Interestingly, in addition to the jobs within manufacturing created by automation, growth in service industries – such as business consulting, engineering firms, and transportation and logistics firms – led to the outsourcing of jobs from manufacturers to these other sectors. Part of the decline in manufacturing’s share of employment was simply a shift in employment to these new industries, as companies utilized outsourcing to focus on their core manufacturing operations.)

At the same time, international trade liberalization grew and U.S. companies found themselves competing with firms all over the world, many of whom faced lower labor costs and environmental standards. In addition, U.S. exports were relatively more expensive due to the strong value of the dollar. Trade liberalization policies beginning in the 1980s (e.g., Canada-U.S. Free Trade Agreement, North American Free Trade Agreement, creation of the World Trade Organization) exacerbated global competition, such that automation wasn’t enough for U.S. firms to compete. Firms moved their manufacturing operations to lower cost places in the world. Trade liberalization accelerated during the 2000s with a series of bilateral trade agreements with countries in Latin and South America and Southeast Asia. Trade and globalization, then, is largely the cause of the decline in manufacturing employment share realized since the 1970s.3

The decline in manufacturing’s importance to the national economy is reflected in the Heartland, though not as severely. While manufacturing’s share of employment declined at an annualized rate of 2.4 percent over the last 50 years, the only Heartland state to realize a higher rate of decline was Illinois at 2.5 percent. Manufacturing still represents over ten percent of employment in the following Heartland states: Alabama, Arkansas, Indiana, Kansas, Kentucky, Michigan, Ohio, and Wisconsin.4

Total manufacturing employment in the Heartland in 2019 was 6.6 million, down from 8.1 million in 2001. Food and beverage manufacturing subsectors actually grew by 62,000 jobs during this period. Computer and electronic products, transportation equipment, printing and related supporting activities, machinery and primary metal manufacturing saw the greatest loss of jobs, though apparel, textile mills, leather and applied products, textile product mills, and printing and related supporting activities manufacturing realized the greatest rates of decline.5

Manufacturing Particularly Impacted by COVID-19 Pandemic

COVID-19 exposed several vulnerabilities in U.S. manufacturing. First, there were disruptions in the supply chains, as Chinese factories were idled well beyond the two-week Lunar New Year holiday. Second, the rapid spread of the coronavirus in the U.S. also led to the closure of manufacturing facilities producing non-essential products, as well as a few facilities deemed essential due to coronavirus spreading among workers. With the idling of most of the world’s manufacturing and widespread “shelter at home” orders in place, demand for intermediate and final goods plummeted, further frustrating the U.S. manufacturing industry.

China’s initial response to the novel coronavirus in late January corresponded with the Lunar New Year, a 15-day holiday during which factories shut down. Since U.S. manufacturers anticipate this annual holiday, they customarily order sufficient inventory to sustain operations with minimal impact during the Lunar New Year. As the Chinese government continued to push back the opening of Chinese factories week after week, American manufacturers faced input shortages and had to scramble to find parts – using existing inventories designated for spare and after-sale parts, or find alternative suppliers, if possible. Delays in manufacturing typically do not manifest themselves immediately. Rather, manufacturing delays will show up in several months, after existing inventories of product in warehouses and in transit are depleted and before new product can be produced and delivered. It may take 6 months or more before factories return to full capacity, and then another month or two before product is distributed out through retailers, for example. The timeline, then for, recovery and stabilization of manufacturing output could be 8 months or more from the time of shutdown. 6

China is deeply embedded in the global supply chain of products. This is illustrated by the large volume of trade between China and the US. In 2019 (during a trade war with China), nearly 20 percent of all imports to the U.S. came from China (over $452 billion), while 6 percent of U.S. exports went to China (over $106 billion). Focusing more specifically on manufacturing exports, 25 percent of U.S. manufacturing exports went to China. Only 19 percent of Heartland manufacturing exports went to Asia.7

But even if manufacturers were able to find the necessary parts to further production, manufacturers of non-essential goods were likely shutdown to prevent spreading the coronavirus among workers. Non-essential manufacturers are predominantly durable goods manufacturers. Several livestock slaughter facilities, deemed essential, were also shutdown because of high transmission of coronavirus amount workers.8

Durable goods manufacturers, in particular, are also facing reduced demand for consumer and industrial goods during the COVID-19 pandemic. This is understandable given that most households are facing reduced income from lost hours and/or layoffs, so that buying “big ticket” items like cars, furniture, and electronics are low priority. And many factories around the world have been idled to prevent the spread of the coronavirus. The collapse of the oil and gas industry, partly driven by low demand for fuel, is also contributing to the decline in durable manufacturing. Many believe that these manufacturers will be impacted most by the pandemic, and some worry about the long-term solvency of key firms coming out of this situation.9 Caterpillar announced that it is considering closing plants in Germany, while PPG Industries announced cut backs to planned capital investments, and Harley-Davidson is suspending a share buyback program and cutting shareholder dividends. These are efforts to conserve cash-on-hand and/or minimize spending in response to the COVID-19 pandemic’s impact on the demand for their products.10

Implications for Heartland Manufacturing

It is important to note that manufacturing, despite job losses and a decline in relative importance, remains a significant employer in the Heartland, and it represents the largest industry in the region by value of production. Manufacturing remains a critical component of the Heartland’s economy, and more importantly, it is a key driver of prosperity in the region due to its export orientation.

The COVID-19 pandemic has exposed weaknesses in the industry, though communities and corporate leadership can examine and grow through rehabilitation. For example, it has been noted that Chinese manufacturing is the central player for most manufacturing in the world; coming out of the pandemic, U.S. manufacturers should re-evaluate their supply chains considering risk management in addition to cost minimization considerations. Diversification of supply chains can mitigate regionalized interruptions, such as the shutdown of Chinese manufacturers in February, 2020. The persistence of manufacturing in the Heartland suggests that suppliers likely exist and making supply chain linkages strengthens the industry. It could also lead to additional economic growth through multiplier effects. Local and regional economic development organizations (EDOs) can play an important role aiding manufacturers to identify U.S.-based suppliers.

Manufacturing facilities are also being forced to evaluate their production mix and processes, and this is an opportunity for innovation. Because social distancing requirements will likely remain for some time, facilities need to consider how to reopen while maintaining precautions and appropriate distancing to protect the health of their workers. This is a prime opportunity for manufacturers to consider cost-saving automation or other innovations to their production process and facility.

Furthermore, some industries have modified their production line to deliver personal protection equipment, medical devices, or sanitization products. This has led firms to form new partnerships (e.g., General Motors working with Ventec to produce ventilators) and innovations (e.g., Dyson’s CoVent). EDOs and institutions of higher education can serve as match-makers and collaborative partners, helping manufacturers to identify new products and processes.

The Heartland region still maintains a comparative advantage for manufacturing through its dense transportation networks and access to world markets, and its proximity to natural resources. Even as alternative fuels become more plentiful and cost-effective, the Heartland remains the energy supplier for the U.S. with wind, solar, oil and gas developments occurring throughout the region. Additionally, other mineral requirements, such as iron, gypsum and high quality silica, are abundant.

While the COVID-19 pandemic poses challenges for manufacturing, hope remains for this industry. Through innovation, new products and collaboration with supporting institutions, manufacturers can leverage the region’s assets and continue to foster economic prosperity throughout the region.

ENDNOTES

- Chmura Economics and Analytics. JobsEQ. Gross Domestic Product data as of 2018. Employment data as of 2019Q4.

- Lazette, Michelle Park. (2020, March 18). “Manufacturing Under Pressure.” Federal Reserve Bank of Cleveland, https://www.clevelandfed.org/manufacturing

- Ibid.

- Author’s calculations using data from the U.S. Department of Commerce, Bureau of Economic Analysis, Total Full-Time and Part-time Employment by SIC industry (1969-2000) or NAICS Industry (2001-2018). The decline between 2000 and 2001 is due to the change in industry classifications between SIC and NAICS.

- Author’s calculations using data from Chmura Economics and Analytics. JobsEQ. Gross Domestic Product data as of 2018. Employment data as of 2019Q4.

- Wharton Business Daily. (2020, March 17). “Coronavirus and Supply Chain Disruption: What Firms Can Learn.” https://knowledge.wharton.upenn.edu/article/veeraraghavan-supply-chain/

- Trade statistics computed using data from U.S. Department of Commerce, International Trade Administration, Global Patterns of U.S. Merchandise Trade and State-by-State Exports to a Selected Market. https://tse.export.gov

- Reiley, Laura. (2020, April 28). “In One Month, the Meat Industry’s Supply Chain Broke. Here’s What You Need to Know.” *The Washington Post.* https://www.washingtonpost.com/business/2020/04/28/meat-industry-supply-chain-faq/

- Sorensen, Jeff & Bono, Bobby. (2020). “COVID-19: What It Means for Industrial Manufacturing.” PwC, https://www.pwc.com/us/en/library/covid-19/coronavirus-impacts-industrial-manufacturing.html

- Hufford, Austen & Tita, Bob. (2020, April 28). “Manufacturers Hit a Wall as Coronavirus Saps Demand.” *The Washington Post.* https://www.wsj.com/articles/manufacturers-hit-a-wall-as-coronavirus-saps-demand-11588087742