Executive Summary

America’s geography of innovation is in the midst of change.

The heartland, the world’s leading center of innovation during the industrial age, lost that distinction around the 1960s to coastal high-tech clusters like Silicon Valley and Boston’s Route 128. But emerging digital technologies and the growth of venture capital investment in high-tech startups have reignited innovation in the heartland. At the same time, the coasts have come up against a crisis of affordable housing and other limits.

The heartland also benefits from the changing nature of innovation. Until recently, high-tech innovation was focused on the creation of new devices and capabilities, like laptop computers, smart phones, biotechnologies, and social media. Many of the products were then manufactured elsewhere, typically in other countries. Today’s exciting technological frontiers involve the application of cutting-edge developments in electrification, advanced mobility, artificial intelligence, advanced materials, and robotics to advanced manufacturing. The heartland stands to benefit because it still excels at making things.

Our research used detailed data on the geography of venture capital investment, a key measure of investment in commercially relevant technology, to quantify and map the change in America’s innovation system and get a better sense of how the heartland stacks up against other parts of the country.

Key Findings

These findings stand out:

- Venture capital investment in the heartland has more than tripled over the past decade to $55 billion. Nearly three-quarters of heartland metros now attract venture capital investment.

- The heartland is home to significant startup ecosystems. Austin, Texas and Chicago rank among the nation’s leading startup centers. Minneapolis-St. Paul, Dallas, Houston, and Columbus, Ohio rank among the nation’s top 20 centers for venture investment. Nashville, Tennessee ranked fifth nationally in venture investment behind only the Bay Area, New York, Boston, and Los Angeles, according to a separate ranking from early 2023.

- Columbus, Ohio, Birmingham, Alabama, Milwaukee, and Oklahoma City all register in the top 20 large metros on venture capital investment growth, while Grand Rapids, Michigan and Indianapolis rank among the top 20 large metros for growth in venture capital deals.

- Austin, Texas and Chicago have levels of venture capital investment that are comparable to Silicon Valley’s in 1995; four heartland metros have levels that are comparable to Boston’s in 1995; and six have levels that are comparable to Washington, D.C.’s three decades ago.

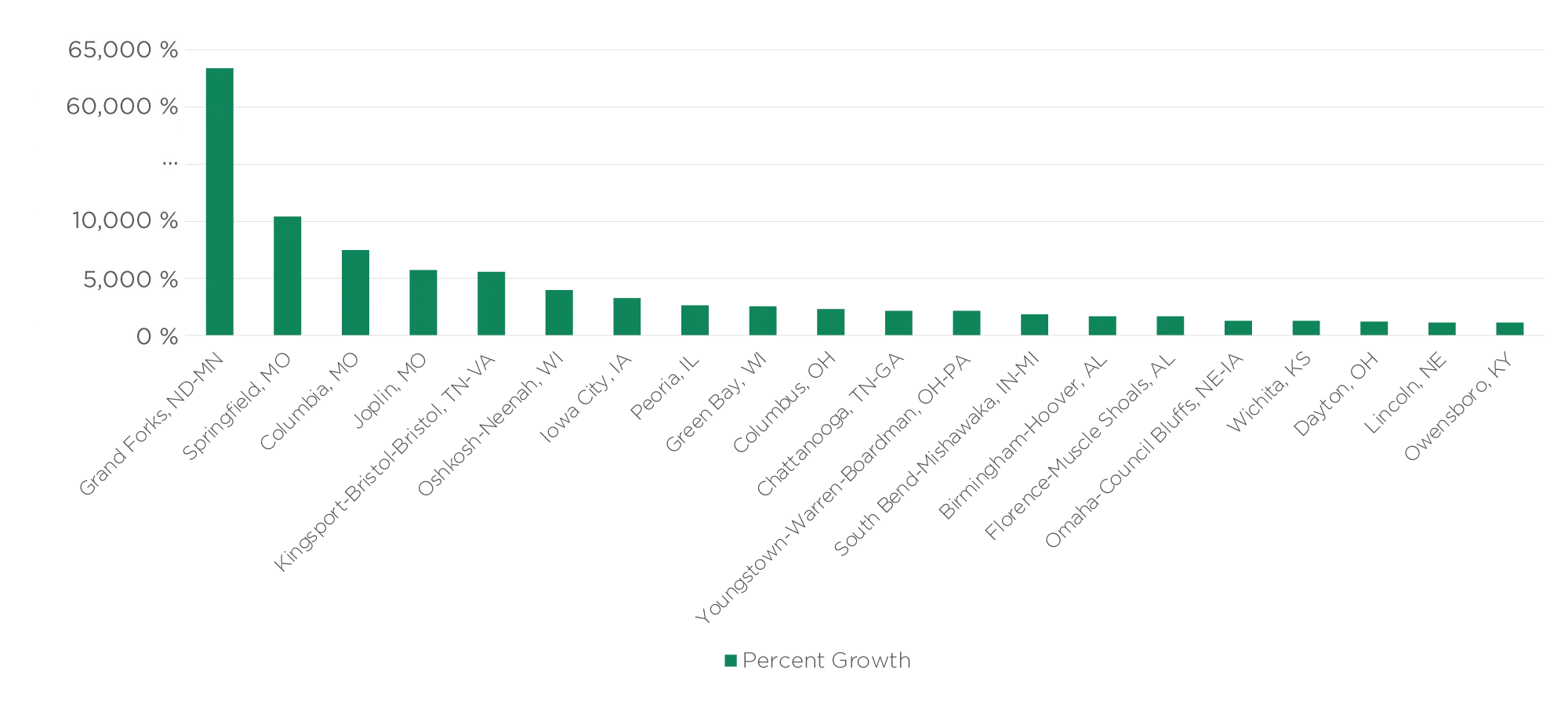

- Smaller heartland metros have also seen significant growth in venture capital investment. Grand Forks, North Dakota; Springfield, Columbia and Joplin, Missouri; Kingsport-Bristol, Tennessee; and Oshkosh-Neenah, Wisconsin all number among the top 20 smaller metros for venture capital growth.

- Heartland college towns have seen significant growth in venture capital investment. These include Ann Arbor, Michigan (University of Michigan), Madison, Wisconsin (University of Wisconsin), Lincoln, Nebraska (University of Nebraska), Columbia, Missouri (University of Missouri), South Bend, Indiana (University of Notre Dame), Grand Forks, North Dakota (University of North Dakota) and Fayetteville, Arkansas (University of Arkansas), to name just a few.

The massive growth in venture capital over the past decade has gone hand in hand with the geographic spread of innovative activity and startup ecosystems. While venture capital and the innovation it supports remains concentrated in established tech hubs, viable high-tech startup ecosystems are now found in growing numbers of heartland communities, from its big cities to its small college towns. The growth of these ecosystems is not just important for the region, but critical for America’s economic future and essential to its prosperity.

A New Model of Industry-Transforming Innovation

To benefit from this shift and make the most of the trend, our research outlines a series of strategic recommendations for leaders across the nation, but specifically for those in the heartland.

Focus on Entrepreneurs and Ecosystems: Developing local innovation and entrepreneurial ecosystems is a long game. It requires a deliberate economic development strategy that shifts the emphasis from traditional industrial recruitment to building the underlying capacities that innovators, entrepreneurs, and startups need. Key to this is identifying potentially successful entrepreneurs and entrepreneurial startups and building networks to support them. That requires an inclusive ecosystem that enables entrepreneurs and innovators of all backgrounds, across all types of industries, to succeed and thrive.

Develop and Attract Entrepreneurial Talent: Entrepreneurial talent – the ability to define and implement commercial priorities – is scarce, critically important, and distinct from technological talent. Programs that work with existing entrepreneurs, universities and colleges can help identify and develop it. Most regions have diasporas of entrepreneurs that can be lured back or tapped for advice, investments and other kinds of support.

Turn Universities into Ecosystem Anchors: Research universities develop new technologies and intellectual property that often form the basis for startups. The heartland is home to nearly 40% of the nation’s leading-edge research universities. Unfortunately, many, if not most, underperform when it comes to commercializing their research. Going forward, universities and state and local governments must make technology transfer, commercialization, and the generation of startups key priorities.

Build Up College Towns: The region must place more emphasis on strategic economic development centered on college towns. These are not just places for young people to get an education and go on to careers elsewhere. They can become talent magnets and anchors of the innovation economy. Almost every leading tech and startup hub grew out of a college town. Palo Alto’s Stanford University catalyzed San Francisco and the Bay Area’s tech industries; Cambridge’s Harvard and MIT helped create Boston’s fabled Route 128; and Austin is home to the University of Texas. The heartland has dozens of college towns that could evolve into bigger and better innovation and startup ecosystems.

Pave the Way for Industry-Transforming Innovation: The heartland has an opportunity to pursue a powerful new model of technology-based economic development – one that does not just generate new innovations but applies them to the upgrading of key manufacturing industries. The heartland has more than half of the nation’s manufacturing employment, and many of its leading universities are close to its manufacturing centers. But forging this new model will require collaborations across business, academic, government and civic institutions.

Tap into Federal Funding Initiatives: The federal government has recognized the importance of this ongoing technological shift by enacting legislation to move toward “placed-based industrial policy.” This is part of an overarching effort to rebuild America’s advanced manufacturing capability and reduce dependence on foreign imports of key technologies. To this end, it has provided some $2 trillion in funding through programs like the CHIPS and Science Act, and the National Science Foundation’s Regional Innovation Engines initiative.

To secure and use this funding, heartland communities must build partnerships locally and regionally – in some cases spanning multiple communities, metro areas and states. The region should consider creating an overarching body – a Heartland Innovation Council – made up of the CEOs of large companies, venture capitalists, entrepreneurs, university presidents and the leaders of major philanthropies –to better align its capabilities with national priorities.

Introduction

Technological innovation has long been the driving force of economic growth.1 And for much of the nineteenth and twentieth centuries, America’s heartland region was home to the world’s most technologically advanced manufacturing industries.

There was Detroit’s Big Three automotive manufacturers; rubber and tires in Akron, Ohio; steel in Pittsburgh and Youngstown, Ohio; glass in Corning, New York and Toledo, Ohio; and the automotive supplier complexes of Cleveland and Buffalo, New York. Corporations like Westinghouse in Pittsburgh and Motorola in Chicago dominated electronics; office furniture was in Grand Rapids, Michigan; and the consumer goods giant Procter & Gamble grew in Cincinnati.

By the mid-twentieth century, the region had the world’s largest complex of advanced corporate research and development laboratories, helping pave the way toward the rise of the knowledge economy.2 This broad, technology-intensive industrial complex underpinned some of the highest incomes and living standards in the world.

But over the past 75 years, innovation that drives economic growth and the institutions that support it have changed, causing dramatic shifts in its geography.3 One after another, the heartland’s industries stagnated or moved to other parts of the country and ultimately offshore. The region fell into a protracted period of deindustrialization and decline.4

The geography of innovation shifted to coastal high-tech hubs like California’s Silicon Valley and Cambridge-Boston. Anchored by great research universities and fueled by venture capital, these complexes rolled out pathbreaking, industry-defining innovations, from semiconductors, computers, software and mobile devices to biotechnology, the Internet, e-commerce, social media, and artificial intelligence.5 Between 2005 and 2017, just five metropolitan areas – San Francisco and San Jose, California, Boston, Seattle, and San Diego – accounted for more than 90% of growth in the high- tech innovation sector. Fully a third of America’s innovation jobs were in just 16 of its more than 3,000 counties.6

The magnitude of this shift can be seen by simply comparing America’s leading companies with those of a half century ago. In 1965, America’s 10 largest companies were General Motors, Exxon, Ford, General Electric, Mobil, Chrysler, U.S. Steel, Texaco, IBM and Gulf Oil.7 Today, the top 10 by market capitalization are Apple, Microsoft, Alphabet (the parent company of Google), Amazon, Nvidia (AI computing), Tesla, Berkshire Hathaway, Meta (the parent of Facebook), Visa and United Health, though Walmart tops Amazon and Apple in revenue.8 The majority of them began as high-tech startups backed by venture capital.

In recent years, however, the bicoastal geography of high-tech innovation came up against a set of natural limits as skyrocketing real estate prices in superstar cities and tech hubs created a new urban crisis that made it harder for them to attract and retain talent and incubate and scale new ventures.9

By creating a huge global experiment in remote work, the pandemic enabled and accelerated the geographic spread of innovative activity, a process that had been underway for a while, and that AOL founder and venture capitalist Steve Case dubbed “the rise of the rest.”10 Case made an impassioned case for coordinated efforts to help grow and expand new startup ecosystems across the nation.11

The rise of high tech innovation in the heartland heralds an even bigger shift in the nature and geography of innovation, which until fairly recently was mainly focused on the creation of altogether new industries. Some of the most exciting frontiers in innovation today are in manufacturing, which is undergoing a wave of creative destruction – the process that the great economist of innovation Joseph Schumpeter singled out as the underlying force of economic progress, revolutionizing “the economic structure from within, incessantly destroying the old one.”12

Computers, software, artificial intelligence and electrification are radically disrupting many traditional manufacturing industries, and as the part of the country that still actually makes things, the heartland is at the center of this shift. The region has the opportunity to forge a new, more holistic model of technology-based growth by applying these new technologies to transform its existing industries.

But is the heartland prepared to take full advantage of this opportunity? Keeping this question in the front of our minds, our research examines how the heartland stacks up on the changing trajectory and geography of innovation across the United States over the past decade. We developed and analyzed detailed data on the geography of venture capital investment, a key measure of investment in commercially relevant technology, across more than 300 U.S. metropolitan areas and the more than 100 metros that comprise the heartland region.

The remainder of this report is organized as follows. The next section assesses how the heartland stacks up on a variety of metrics for venture capital and startup activity. After that, we summarize the key trends and patterns our research uncovered about the geography of innovation. The last section outlines a strategy for strengthening the heartland’s innovation ecosystems and aligning them with its industrial capabilities in ways that can bolster overall competitiveness and create more balanced economic growth.

How The Heartland Stacks Up

The past decade has seen astronomical growth in venture capital investment, even with the COVID pandemic of 2020-2021. Roughly three-quarters (75.4%) of heartland metros (126 of 167), and nearly 80% (78.3%) of all metros (301 of 384) received venture capital investment in 2019-2021. Venture capital investment in the heartland more than tripled, skyrocketing from roughly $15 billion in 2009-2011 to $55 billion in 2019-2021. All in all, 30 heartland metros – a quarter of those that received venture capital – outpaced the national average for growth in venture capital investment.

Such expansive growth in venture capital has enabled the spread of larger, more functional, and viable startup ecosystems in more places across the country, but especially in the heartland.

The surge has been so substantial that a significant number of metros, including some in the heartland, have levels of venture capital investment that are similar to or even exceed those of Silicon Valley, Boston-Cambridge, New York City, and Washington, D.C. in the mid-1990s (see Figure 1).13

FIGURE 1: NUMBER OF METROS ECLIPSING 1995’S LEADING TECH HUBS

| VENTURE CAPITAL INVESTMENT IN 1995 (MILLIONS OF DOLLARS) | VENTURE CAPITAL INVESTMENT IN 1995 (MILLIONS OF 2020 DOLLARS) | NUMBER OF METROS ABOVE IN 2020 | |

|---|---|---|---|

| Silicon Valley | $1,829 | $3,107 | 11 |

| Boston-Cambridge | $784 | $1,331 | 18 |

| New York City | $512 | $871 | 23 |

| Washington, D.C. | $417 | $708 | 26 |

- Eleven metros across the country have levels of venture capital investment that exceed Silicon Valley’s in 1995 ($3.1 billion in 2020 dollars). The list includes Austin, Texas and Chicago in the heartland, as well as New York City and Boston- Cambridge, each with more than five times as much as Silicon Valley back then; Los Angeles with four times as much; San Diego, with twice as much; and Washington D.C., and Philadelphia with similar amounts.

- Eighteen metros, including four in the heartland, have as much or more venture capital investment as Boston-Cambridge did in 1995 ($1.3 billion in 2020 dollars). These include Minneapolis-St. Paul and Dallas in the heartland, as well as Atlanta, Miami, Denver, Salt Lake City, and Phoenix.

- Twenty-three metros, including six in the heartland, that have as much or more venture capital investment as New York did in 1995 ($870 million in 2020 dollars). These are Houston and Columbus, Ohio in the heartland, as well as Portland, Oregon, Raleigh and Durham, North Carolina. And 26 metros have as much as Washington, D.C. did in 1995 ($708 million in 2020 dollars).

Despite the impressive rise of venture capital investment in the heartland, the region still lags behind national trends. While venture capital investment rose by 374%, it increased by even more across the nation as a whole, surging from roughly $100 billion in 2009-11 to more than $600 billion by 2019-21 (see Figure 2), or 580%.

FIGURE 2: GROWTH IN VENTURE CAPITAL INVESTMENT IN THE HEARTLAND VERSUS THE UNITED STATES

| HEARTLAND | UNITED STATES | ||

|---|---|---|---|

| Venture Capital Deals | Number | 6,955 | 43,894 |

| Share | 15.8% | ||

| Venture Capital Investment | Billions | $55.0 | $611.6 |

| Share | 9.0% | ||

| Change | Billions | $40.3 | $506.1 |

| Percent | 374% | 580% |

FIGURE 3: GROWTH IN VENTURE CAPITAL INVESTMENT, 2009-11 TO 2019-21

FIGURE 4: GROWTH IN VENTURE CAPITAL INVESTMENT FOR HEARTLAND METROS

| HEARTLAND RANK | OVERALL RANK | METRO | PERCENT GROWTH |

|---|---|---|---|

| 1 | 2 | Grand Forks, ND-MN | 63,417% |

| 2 | 9 | Springfield, MO | 10,395% |

| 3 | 10 | Columbia, MO | 7,478% |

| 4 | 12 | Joplin, MO | 5,707% |

| 5 | 13 | Kingsport-Bristol-Bristol, TN-VA | 5,577% |

| 6 | 21 | Oshkosh-Neenah, WI | 3,973% |

| 7 | 25 | Iowa City, IA | 3,199% |

| 8 | 28 | Peoria, IL | 2,574% |

| 9 | 29 | Green Bay, WI | 2,499% |

| 10 | 31 | Columbus, OH | 2,283% |

| 11 | 35 | Chattanooga, TN-GA | 2,125% |

| 12 | 37 | Youngstown-Warren-Boardman, OH-PA | 2,102% |

| 13 | 42 | South Bend-Mishawaka, IN-MI | 1,792% |

| 14 | 44 | Birmingham-Hoover, AL | 1,661% |

| 15 | 45 | Florence-Muscle Shoals, AL | 1,648% |

| 16 | 54 | Omaha-Council Bluffs, NE-IA | 1,286% |

| 17 | 55 | Wichita, KS | 1,279% |

| 18 | 57 | Dayton, OH | 1,139% |

| 19 | 58 | Lincoln, NE | 1,136% |

| 20 | 59 | Owensboro, KY | 1,114% |

Still, the growth in venture capital in some parts of the heartland has been astonishing (see Figure 4).

- Grand Forks, North Dakota posted an astounding growth rate of more than 63,000% – the second fastest of any metro in the country.

- Four other heartland metros saw growth rates of more than 5,000%: Springfield (10,395%), Columbia (7,478%) and Joplin, Missouri (5,707%); and Kingsport, Tennessee (5,577%).

- Seven additional metros saw gains of between 2,000% and 4,000%: Oshkosh, Wisconsin (3,973%); Iowa City, Iowa (3,199%); Peoria, Illinois (2,574%); Green Bay, Wisconsin (2,499%), Columbus, Ohio (2,283%); Chattanooga, Tennessee (2,125%); and Youngstown, Ohio (2,102%).

- Ten other heartland metros saw growth of between 1,000 and 2,000%, including South Bend, Indiana (1,792%); Florence-Muscle Shoals, Alabama (1,648%); Omaha, Nebraska (1,286%); Wichita, Kansas (1,279%); Dayton, Ohio (1,139%); Lincoln, Nebraska (1,136%); and Owensboro, Kentucky (1,114%).

Table 1: Growth In Venture Capital Investment For Large Metros

| LARGE METRO RANK | OVERALL RANK | METRO | PERCENT GROWTH |

|---|---|---|---|

| 1 | 4 | Fresno, CA | 25,090% |

| 2 | 19 | Riverside-San Bernardino-Ontario, CA | 4,446% |

| 3 | 31 | Columbus, OH | 2,283% |

| 4 | 44 | Birmingham-Hoover, AL | 1,661% |

| 5 | 46 | Virginia Beach-Norfolk-Newport News, VA-NC | 1,595% |

| 6 | 61 | New York-Northern New Jersey-Long Island, NY-NJ-PA | 1,089% |

| 7 | 63 | Sacramento-Arden-Arcade-Roseville, CA | 1,039% |

| 8 | 67 | Milwaukee-Waukesha-West Allis, WI | 915% |

| 9 | 71 | Las Vegas-Paradise, NV | 817% |

| 10 | 74 | Phoenix-Mesa-Scottsdale, AZ | 769% |

| 11 | 76 | Seattle-Tacoma-Bellevue, WA | 736% |

| 12 | 78 | Los Angeles-Long Beach-Santa Ana, CA | 730% |

| 13 | 83 | Salt Lake City, UT | 708% |

| 14 | 84 | Oklahoma City, OK | 706% |

| 15 | 86 | San Francisco-Oakland-Fremont, CA | 698% |

| 16 | 87 | Jacksonville, FL | 686% |

| 17 | 88 | Buffalo-Niagara Falls, NY | 668% |

| 18 | 90 | Miami-Fort Lauderdale-Pompano Beach, FL | 625% |

| 19 | 91 | Boston-Cambridge-Quincy, MA-NH | 609% |

| 20 | 95 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | 589% |

Four heartland metros rank among the top 20 large metros on growth in venture capital investment (see Table 1).

- Columbus, Ohio is third (with 2,283% growth); Birmingham, Alabama fourth (1,661%); Milwaukee is eighth (915%); and Oklahoma City fourteenth (706%).

- Fresno, California, which likely benefits from spillover growth from both San Francisco and Los Angeles, is the top ranked large metro with growth of more than 25,000%, followed by Riverside, California (4,400%), which is also close to Los Angeles. Virginia Beach, Virginia is fifth with growth of more than 1,500%.

- The rest of the top 20 includes superstar metros like New York City (1,089%) and Los Angeles (730%); Sun Belt hot spots like Las Vegas (817%) and Phoenix (769%); established startup hubs like Seattle (with 736%), San Francisco (698%), and Boston (609%); and emerging tech hubs like Salt Lake City (708%) and Miami (625%). Other metros that rank among the top 20 are Sacramento, California which also likely benefits from spillover growth from San Francisco (1039%), as well as Jacksonville, Florida (688%), Buffalo, New York (668%), and Philadelphia (589%).

Table 2: Growth In Venture Capital Investment For Smaller Metros

| SMALLER METRO RANK | OVERALL RANK | METRO | PERCENT GROWTH |

|---|---|---|---|

| 1 | 1 | Bremerton-Silverdale, WA | 88,620% |

| 2 | 2 | Grand Forks, ND-MN | 63,417% |

| 3 | 3 | Naples-Marco Island, FL | 51,648% |

| 4 | 5 | Asheville, NC | 24,721% |

| 5 | 6 | Cheyenne, WY | 19,914% |

| 6 | 7 | Myrtle Beach-Conway-North Myrtle Beach, SC | 12,272% |

| 7 | 8 | Huntington-Ashland, WV-KY-OH | 11,268% |

| 8 | 9 | Springfield, MO | 10,395% |

| 9 | 10 | Columbia, MO | 7,478% |

| 10 | 11 | Lancaster, PA | 6,438% |

| 11 | 12 | Joplin, MO | 5,707% |

| 12 | 13 | Kingsport-Bristol-Bristol, TN-VA | 5,577% |

| 13 | 14 | Norwich-New London, CT | 5,451% |

| 14 | 15 | Florence, SC | 5,000% |

| 15 | 16 | Dover, DE | 4,889% |

| 16 | 17 | Binghamton, NY | 4,868% |

| 17 | 18 | Modesto, CA | 4,640% |

| 18 | 20 | Santa Fe, NM | 4,018% |

| 19 | 21 | Oshkosh-Neenah, WI | 3,973% |

| 20 | 22 | Medford, OR | 3,649% |

Six heartland metros number among the top 20 smaller metros for growth in venture capital investment (see Table 2). This reflects the enormous progress they have made, rising from near nothing a decade ago.

- Grand Forks, North Dakota is second; Springfield, Columbia, and Joplin, Missouri are eighth, ninth, and 11th; Kingsport, Tennessee is 12th and Oshkosh, Wisconsin 19th.

- Bremerton, Washington takes first place with more than 80,000% growth (88,620%), Naples, Florida is third (51,648%), Asheville, North Carolina is fourth (24,721%), Cheyenne, Wyoming fifth (19,914%), Myrtle Beach, South Carolina sixth (12,272%) and Huntington, West Virginia seventh (11,268%).

- Rounding out the top 20 are Lancaster, Pennsylvania (6,438%), Norwich, Connecticut (5,451%), Florence, South Carolina (5,000%), Dover, Delaware (4,889%), Binghamton, New York (4,868%), Modesto, California (4,640%), Santa Fe, New Mexico (4,018%) and Medford, Oregon (3,649%).

Bigger Isn’t Necessarily Better

Larger cities and metros are likely to have higher levels of venture capital investments simply by virtue of their size. We control for this by looking at trends in venture capital on a per capita basis.

FIGURE 5: PER CAPITA VENTURE CAPITAL INVESTMENT

The leading heartland metros on this metric include a mix of established tech hubs, large metros and college towns (see Table 3).

- Austin, Texas, the home of the flagship institution of the University of Texas, leads with more than $5,000 ($5,276) in venture capital investment per capita.

- Seven other heartland metros, mainly college towns, have between $1,000 and $2,000 in venture capital investment per capita: Ann Arbor, Michigan (University of Michigan) with $1,937, Columbia, Missouri (University of Missouri) with $1,515, Minneapolis-St. Paul (University of Minnesota) with $1,408, Columbus, Ohio (The Ohio State University) with $1,376, Madison, Wisconsin (University of Wisconsin) with $1,299, Chicago (University of Chicago and Northwestern University) with $1,266 and Lincoln, Nebraska (University of Nebraska) with $1,016.

- Eight more heartland metros have between $500 and $1,000 in venture capital investment per capita, and all but one hosts a university. These include Nashville, Tennessee (Vanderbilt University) with $987, Grand Forks, North Dakota (University of North Dakota) with $911, Midland, Texas with $819, Bloomington, Indiana (Indiana University) with $755, and Dallas (home to SMU, University of North Texas, and the University of Texas at Dallas) with $674. St. Louis (Washington University) and Pine Bluff, Arkansas (University of Arkansas Pine Bluff) each have $544, and Iowa City, Iowa (University of Iowa) has $505.

- Rounding out the top 20 heartland metros are Lafayette, Indiana (Purdue University) with $491, Houston (home to Rice University, University of Houston and more) with $463, Champaign- Urbana, Illinois (University of Illinois) with $417 and Lexington, Kentucky (University of Kentucky) with $410.

Table 3: Per Capita Venture Capital Investment For Heartland Metros

| HEARTLAND METRO RANK | OVERALL RANK | METRO | INVESTMENT PER CAPITA |

|---|---|---|---|

| 1 | 7 | Austin-Round Rock, TX | $5,276 |

| 2 | 22 | Ann Arbor, MI | $1,937 |

| 3 | 28 | Columbia, MO | $1,515 |

| 4 | 31 | Minneapolis-St. Paul-Bloomington, MN-WI | $1,408 |

| 5 | 32 | Columbus, OH | $1,376 |

| 6 | 34 | Madison, WI | $1,299 |

| 7 | 36 | Chicago-Naperville-Joliet, IL-IN-WI | $1,226 |

| 8 | 43 | Lincoln, NE | $1,016 |

| 9 | 44 | Nashville-Davidson-Murfreesboro-Franklin, TN | $987 |

| 10 | 45 | Grand Forks, ND-MN | $911 |

| 11 | 48 | Midland, TX | $819 |

| 12 | 50 | Bloomington, IN | $755 |

| 13 | 53 | Dallas-Fort Worth-Arlington, TX | $674 |

| 14 | 60 | St. Louis, MO-IL | $544 |

| 15 | 61 | Pine Bluff, AR | $544 |

| 16 | 63 | Iowa City, IA | $505 |

| 17 | 65 | Lafayette, IN | $491 |

| 18 | 67 | Houston-Sugar Land-Baytown, TX | $463 |

| 19 | 71 | Champaign-Urbana, IL | $417 |

| 20 | 72 | Lexington-Fayette, KY | $410 |

| United States Total | $1,843 | ||

Five heartland metros rank among the top 20 large metros on per capita venture capital investment (see Table 4). Austin, Texas ranks seventh, Minneapolis- St. Paul, 14th, Columbus, Ohio 15th, Chicago, 18th and Nashville, Tennessee 20th.

San Francisco tops the list of large metros on this metric with more than $35,000 in per capita venture capital investment, followed by San Jose, California in Silicon Valley with nearly $25,000. Next In line are the established tech hubs of Boston-Cambridge with $12,581; and San Diego with $5,935 per capita. The rest of the top 20 includes large superstar cities that have grown their startup activity like New York City ($4,389) and Los Angeles ($3,321); established and emerging tech hubs like Seattle ($4,109), Salt Lake City ($3,872), Denver ($2,344), Washington, D.C. ($1,670), Raleigh-Cary in North Carolina’s Research Triangle ($1,629), and Portland, Oregon ($1,149); along with larger Frostbelt metros like Chicago and Philadelphia ($1,584), and Sunbelt centers like Atlanta ($1,363) and Miami ($1,228).

Table 4: Per Capita Venture Capital Investment For Large Metros

| LARGE METRO RANK | OVERALL RANK | METRO | INVESTMENT PER CAPITA |

|---|---|---|---|

| 1 | 1 | San Francisco-Oakland-Fremont, CA | $35,950 |

| 2 | 2 | San Jose-Sunnyvale-Santa Clara, CA | $24,788 |

| 3 | 4 | Boston-Cambridge-Quincy, MA-NH | $12,581 |

| 4 | 6 | San Diego-Carlsbad-San Marcos, CA | $5,935 |

| 5 | 7 | Austin-Round Rock, TX | $5,276 |

| 6 | 9 | New York-Northern New Jersey-Long Island, NY-NJ-PA | $4,389 |

| 7 | 13 | Seattle-Tacoma-Bellevue, WA | $4,109 |

| 8 | 14 | Salt Lake City, UT | $3,872 |

| 9 | 16 | Los Angeles-Long Beach-Santa Ana, CA | $3,321 |

| 10 | 19 | Denver-Aurora, CO | $2,344 |

| 11 | 25 | Washington-Arlington-Alexandria, DC-VA-MD-WV | $1,670 |

| 12 | 26 | Raleigh-Cary, NC | $1,629 |

| 13 | 27 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | $1,584 |

| 14 | 31 | Minneapolis-St. Paul-Bloomington, MN-WI | $1,408 |

| 15 | 32 | Columbus, OH | $1,376 |

| 16 | 33 | Atlanta-Sandy Springs-Marietta, GA | $1,363 |

| 17 | 35 | Miami-Fort Lauderdale-Pompano Beach, FL | $1,228 |

| 18 | 36 | Chicago-Naperville-Joliet, IL-IN-WI | $1,226 |

| 19 | 41 | Portland-Vancouver-Beaverton, OR-WA | $1,149 |

| 20 | 44 | Nashville-Davidson-Murfreesboro-Franklin, TN | $987 |

| United States Total | $1,843 | ||

Three heartland metros, all of them college towns, rank among the top 20 smaller metros on per capita venture capital investment (see Table 5).

- Ann Arbor, Michigan is 12th with $1,937; Columbia, Missouri is 15th with $1,515 and Madison, Wisconsin is 18th with $1,299.

- Boulder, Colorado (University of Colorado) takes first place among smaller metros with $13,171; Santa Barbara, Colorado (University of California Santa Barbara) is third with $4,911; Durham, North Carolina (Duke University) is fourth with $4,332; Santa Cruz, California (University of California Santa Cruz) is fifth with $4,192; Burlington, Vermont (University of Vermont) is seventh with $3,350; Provo, Utah (Brigham Young University) is eighth with $3,304; Charlottesville, Virginia (University of Virginia) is tenth with $2,038; New Haven, Connecticut (Yale University) is 14th with $1,762 and Missoula, Montana (University of Montana) is 17th with $1,465.

Table 5: Per Capita Venture Capital Investment For Smaller Metros

| SMALLER METRO RANK | OVERALL RANK | METRO | INVESTMENT PER CAPITA |

|---|---|---|---|

| 1 | 3 | Boulder, CO | $13,171 |

| 2 | 5 | Carson City, NV | $9,734 |

| 3 | 8 | Santa Barbara-Santa Maria-Goleta, CA | $4,911 |

| 4 | 10 | Durham, NC | $4,332 |

| 5 | 11 | Santa Cruz-Watsonville, CA | $4,192 |

| 6 | 12 | Dover, DE | $4,127 |

| 7 | 15 | Burlington-South Burlington, VT | $3,350 |

| 8 | 17 | Provo-Orem, UT | $3,304 |

| 9 | 18 | Reno-Sparks, NV | $2,531 |

| 10 | 20 | Charlottesville, VA | $2,038 |

| 11 | 21 | Bridgeport-Stamford-Norwalk, CT | $1,980 |

| 12 | 22 | Ann Arbor, MI | $1,937 |

| 13 | 23 | Harrisonburg, VA | $1,916 |

| 14 | 24 | New Haven-Milford, CT | $1,762 |

| 15 | 28 | Columbia, MO | $1,515 |

| 16 | 29 | Santa Fe, NM | $1,477 |

| 17 | 30 | Missoula, MT | $1,465 |

| 18 | 34 | Madison, WI | $1,299 |

| 19 | 37 | Fort Collins-Loveland, CO | $1,215 |

| 20 | 38 | Burlington, NC | $1,173 |

| United States Total | $1,843 | ||

The Spiky Nature Of Venture Capital And Innovation

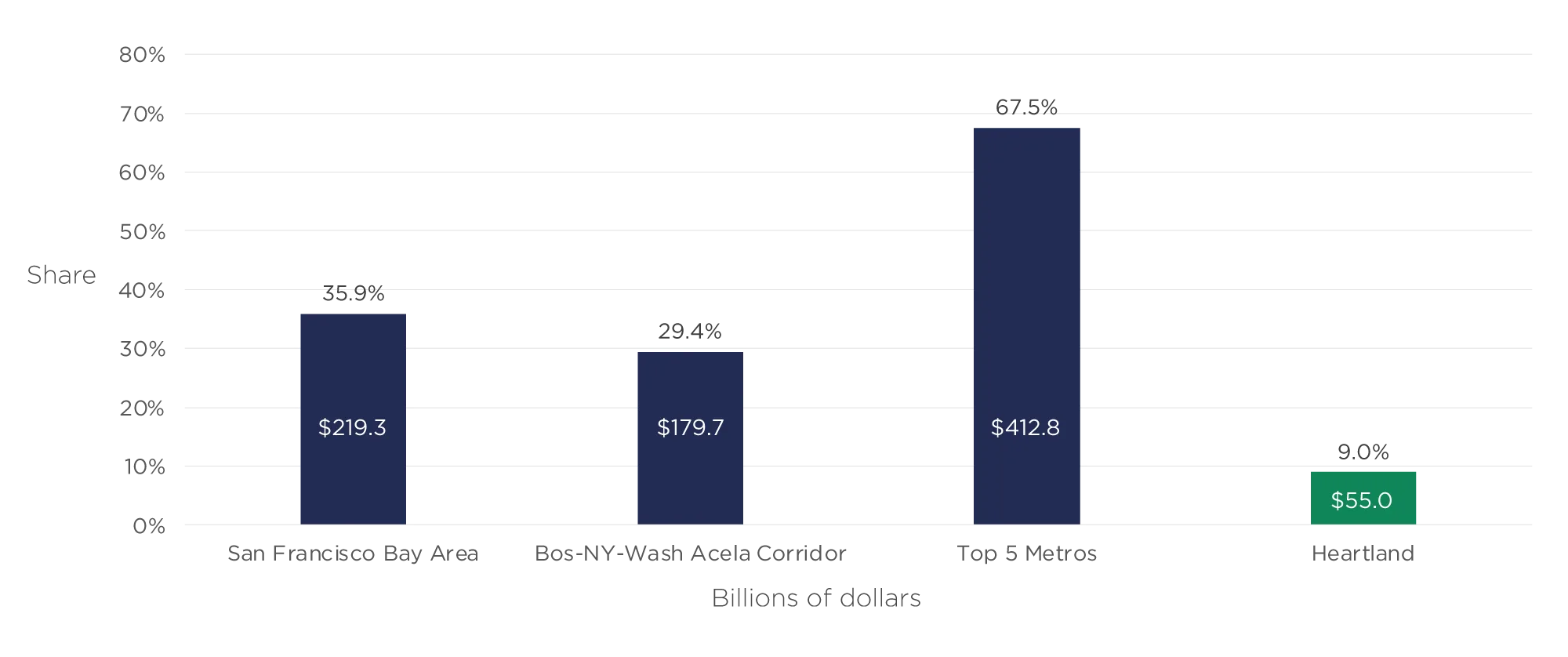

Despite the spread of venture capital investment and startup ecosystems across the nation and its heartland, the overall geography of venture capital remains significantly clustered, concentrated, and spiky.14

The extent to which venture capital dollars and deals are concentrated in just a small number of places is striking.

FIGURE 6: SHARE OF VENTURE CAPITAL INVESTMENT AND DEALS FOR LEADING METROS AND MEGA-REGIONS

| VENTURE CAPITAL INVESTMENT | ||

|---|---|---|

| TOTAL (BILLIONS) | SHARE | |

| San Francisco Bay Area | $219.3 | 35.9% |

| Bos-NY-Wash Acela Corridor | $179.7 | 29.4% |

| Top 5 Metros | $412.8 | 67.5% |

| Heartland | $55.0 | 9.0% |

| United States Total | $611.6 | |

- Just one geographic region – the San Francisco Bay Area, spanning the San Francisco and San Jose metro areas – accounts for nearly four times as much venture capital investment (35.9%) as the entire heartland (9.0%). After declining during the pandemic, the Bay Area’s share of venture capital investment rebounded to 41% in the first quarter of 2023, based in part on its concentration of artificial intelligence startups and talent.15

- The East Coast Acela Corridor spanning Boston, New York City, and Washington, D.C. accounts for three times (29.4%) as much venture capital investment as the heartland.

- Overall, just the top five metros for venture capital – San Francisco, New York City, Boston, SanJose, California and Los Angeles – account for more than two-thirds (67.5%) of venture capital investment across the nation (see Figure 6).16

- Only three U.S. metros saw significant gains in the shares of venture capital they received over the past decade: New York City, which posted by far the largest gain, Los Angeles, and San Francisco. No other metros managed to grow its share of venture capital by even one percentage point.

The heartland actually punches below its weight when it comes to venture capital.

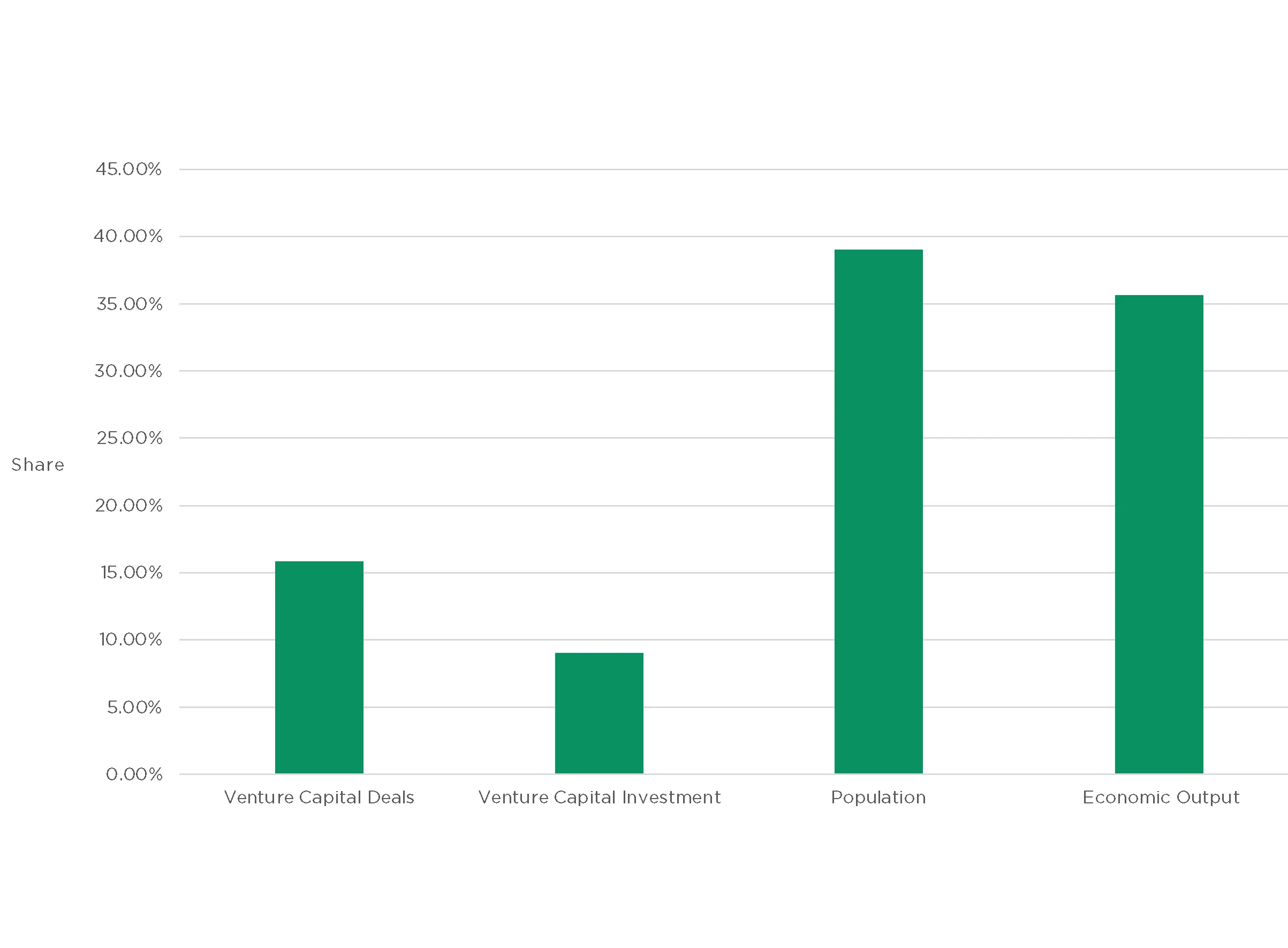

- The entire region accounts for just 9% of overall U.S. venture capital investment and 16% of overall venture capital deals. This is less than the region’s size would seem to warrant. The heartland as a whole is home to 39% of the U.S. population and 36% of its economic output (see Figure 7).

- The heartland’s shares of venture capital investment and deals are actually lower than they were a decade ago (2009-11), when the region accounted for 14% of investment and 17% of deals.

FIGURE 7: VENTURE CAPITAL, POPULATION AND ECONOMIC OUTPUT IN THE HEARTLAND VERSUS THE UNITED STATES

| HEARTLAND | SHARE | |

|---|---|---|

| Venture Capital Deals | 6,955 | 15.8% |

| Venture Capital Investment (billions) | $55.0 | 9.0% |

| Population (millions) | 128.6 | 39.0% |

| Economic Output (trillions) | $9.1 | 36.0% |

FIGURE 8: SHARE OF VENTURE CAPITAL INVESTMENT

FIGURE 9: SHARE OF VENTURE CAPITAL DEALS

Table 6: Share Of Venture Capital Investment For Large Metros

| LARGE METRO RANK | OVERALL RANK | METRO | INVESTMENT (MILLIONS) | SHARE |

|---|---|---|---|---|

| 1 | 1 | San Francisco-Oakland-Fremont, CA | $169,883 | 27.78% |

| 2 | 2 | New York-Northern New Jersey-Long Island, NY-NJ-PA | $87,826 | 14.36% |

| 3 | 3 | Boston-Cambridge-Quincy, MA-NH | $61,798 | 10.10% |

| 4 | 4 | San Jose-Sunnyvale-Santa Clara, CA | $49,460 | 8.09% |

| 5 | 5 | Los Angeles-Long Beach-Santa Ana, CA | $43,847 | 7.17% |

| 6 | 6 | San Diego-Carlsbad-San Marcos, CA | $19,563 | 3.20% |

| 7 | 7 | Seattle-Tacoma-Bellevue, WA | $16,317 | 2.67% |

| 8 | 8 | Austin-Round Rock, TX | $11,787 | 1.93% |

| 9 | 9 | Chicago-Naperville-Joliet, IL-IN-WI | $11,779 | 1.93% |

| 10 | 10 | Washington-Arlington-Alexandria, DC-VA-MD-WV | $10,576 | 1.73% |

| 11 | 11 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | $9,846 | 1.61% |

| 12 | 12 | Atlanta-Sandy Springs-Marietta, GA | $8,214 | 1.34% |

| 13 | 13 | Miami-Fort Lauderdale-Pompano Beach, FL | $7,498 | 1.23% |

| 14 | 14 | Denver-Aurora, CO | $6,884 | 1.13% |

| 15 | 15 | Minneapolis-St. Paul-Bloomington, MN-WI | $5,154 | 0.84% |

| 16 | 16 | Dallas-Fort Worth-Arlington, TX | $5,082 | 0.83% |

| 17 | 17 | Salt Lake City, UT | $4,820 | 0.79% |

| 18 | 19 | Phoenix-Mesa-Scottsdale, AZ | $3,980 | 0.65% |

| 19 | 20 | Houston-Sugar Land-Baytown, TX | $3,262 | 0.53% |

| 20 | 21 | Columbus, OH | $2,921 | 0.48% |

| United States Total | $611,566 | |||

Six heartland metros rank among the top 20 large metros on their shares of venture capital investment (see Table 6).

- Two of them – Austin, Texas and Chicago – make the top 10, in eighth and ninth places respectively, with roughly 2% of the national total each.

- Four more make the top 20: Minneapolis-St. Paul is in 15th place (accounting for 0.84% of the national total); Dallas is in 16th place (0.83%); Houston is 18th (0.53%) and Columbus, Ohio is 19th (0.48%).

- All are far behind San Francisco’s commanding 28%, New York City’s 14% and Boston’s 10% shares of the national total for venture capital investment.

Table 7: Share Of Venture Capital Deals For Large Metros

| LARGE METRO RANK | OVERALL RANK | METRO | DEALS | SHARE |

|---|---|---|---|---|

| 1 | 1 | San Francisco-Oakland-Fremont, CA | 7,271 | 16.56% |

| 2 | 2 | New York-Northern New Jersey-Long Island, NY-NJ-PA | 5,787 | 13.18% |

| 3 | 3 | Los Angeles-Long Beach-Santa Ana, CA | 3,344 | 7.62% |

| 4 | 4 | Boston-Cambridge-Quincy, MA-NH | 2,810 | 6.40% |

| 5 | 5 | San Jose-Sunnyvale-Santa Clara, CA | 2,318 | 5.28% |

| 6 | 6 | Seattle-Tacoma-Bellevue, WA | 1,254 | 2.86% |

| 7 | 7 | Austin-Round Rock, TX | 1,145 | 2.61% |

| 8 | 8 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | 1,129 | 2.57% |

| 9 | 9 | Chicago-Naperville-Joliet, IL-IN-WI | 1,100 | 2.51% |

| 10 | 10 | San Diego-Carlsbad-San Marcos, CA | 1,045 | 2.38% |

| 11 | 11 | Washington-Arlington-Alexandria, DC-VA-MD-WV | 986 | 2.25% |

| 12 | 12 | Miami-Fort Lauderdale-Pompano Beach, FL | 783 | 1.78% |

| 13 | 13 | Denver-Aurora, CO | 776 | 1.77% |

| 14 | 14 | Atlanta-Sandy Springs-Marietta, GA | 695 | 1.58% |

| 15 | 15 | Dallas-Fort Worth-Arlington, TX | 625 | 1.42% |

| 16 | 16 | Houston-Sugar Land-Baytown, TX | 465 | 1.06% |

| 17 | 17 | Minneapolis-St. Paul-Bloomington, MN-WI | 421 | 0.96% |

| 18 | 18 | Phoenix-Mesa-Scottsdale, AZ | 396 | 0.90% |

| 19 | 20 | Portland-Vancouver-Beaverton, OR-WA | 355 | 0.81% |

| 20 | 21 | Salt Lake City, UT | 331 | 0.75% |

| United States Total | 43,894 | |||

The number of venture capital deals is a useful metric, since overall dollar amounts can be easily skewed by a few large investments. When we compare numbers of deals, the percentage shares held by the leading metros are significantly reduced, with San Francisco accounting for roughly 16% of deals compared to nearly 28% of investments. The same heartland metros turn up when we use this metric, but now with slightly higher percentages (see Table 7).

- Austin, Texas and Chicago again crack the top 10 in seventh and ninth places respectively, with roughly 2.5% of the national total each.

- Dallas is 15th; Houston is 16th; and Minneapolis-St. Paul is 17th. They account for roughly 1 to 1.5% of the national total each.

Table 8: Share Of Venture Capital Investment In Smaller Metros

| SMALLER METRO RANK | OVERALL RANK | METRO | INVESTMENT (MILLIONS) | SHARE |

|---|---|---|---|---|

| 1 | 18 | Boulder, CO | $4,329 | 0.71% |

| 2 | 23 | Durham, NC | $2,783 | 0.46% |

| 3 | 25 | Santa Barbara-Santa Maria-Goleta, CA | $2,199 | 0.36% |

| 4 | 26 | Provo-Orem, UT | $2,180 | 0.36% |

| 5 | 29 | Bridgeport-Stamford-Norwalk, CT | $1,894 | 0.31% |

| 6 | 33 | New Haven-Milford, CT | $1,524 | 0.25% |

| 7 | 36 | Reno-Sparks, NV | $1,225 | 0.20% |

| 8 | 37 | Santa Cruz-Watsonville, CA | $1,141 | 0.19% |

| 9 | 39 | Oxnard-Thousand Oaks-Ventura, CA | $982 | 0.16% |

| 10 | 41 | Albany-Schenectady-Troy, NY | $919 | 0.15% |

| 11 | 42 | Madison, WI | $876 | 0.14% |

| 12 | 46 | Burlington-South Burlington, VT | $752 | 0.12% |

| 13 | 47 | Dover, DE | $743 | 0.12% |

| 14 | 48 | Ann Arbor, MI | $721 | 0.12% |

| 15 | 52 | Carson City, NV | $564 | 0.09% |

| 16 | 53 | Boise City-Nampa, ID | $495 | 0.08% |

| 17 | 55 | Charlottesville, VA | $449 | 0.07% |

| 18 | 56 | Trenton-Princeton, NJ | $448 | 0.07% |

| 19 | 57 | Fort Collins-Loveland, CO | $431 | 0.07% |

| 20 | 60 | Santa Rosa-Petaluma, CA | $343 | 0.06% |

| United States Total | $611,566 | |||

Just two heartland metros make the list of score among the top 20 smaller metros on their share of venture capital investment (see Table 8): the college towns of Madison, Wisconsin (11th place with 0.14% of the total) and Ann Arbor, Michigan (14th place with 0.12%).

The list is dotted with other college towns, including Boulder, Colorado (University of Colorado), Durham, North Carolina (Duke University), Santa Barbara, California (University of California-Santa Barbara), New Haven, Connecticut (Yale University), Burlington, Vermont (University of Vermont), Albany, New York (Rensselaer Polytechnic and SUNY-Albany), Charlottesville, Virginia (University of Virginia) and Trenton-Princeton, New Jersey (Princeton University).

Table 9: Share Of Venture Capital Deals For Smaller Metros

| SMALLER METRO RANK | OVERALL RANK | METRO | DEALS | SHARE |

|---|---|---|---|---|

| 1 | 19 | Boulder, CO | 379 | 0.86% |

| 2 | 27 | Durham, NC | 224 | 0.51% |

| 3 | 28 | Provo-Orem, UT | 204 | 0.46% |

| 4 | 28 | Bridgeport-Stamford-Norwalk, CT | 204 | 0.46% |

| 5 | 40 | Madison, WI | 126 | 0.29% |

| 6 | 41 | Santa Barbara-Santa Maria-Goleta, CA | 124 | 0.28% |

| 7 | 41 | New Haven-Milford, CT | 124 | 0.28% |

| 8 | 43 | Dover, DE | 122 | 0.28% |

| 9 | 45 | Ann Arbor, MI | 112 | 0.26% |

| 10 | 54 | Oxnard-Thousand Oaks-Ventura, CA | 80 | 0.18% |

| 11 | 56 | Charlottesville, VA | 77 | 0.18% |

| 12 | 57 | Charleston-North Charleston, SC | 73 | 0.17% |

| 13 | 58 | Boise City-Nampa, ID | 72 | 0.16% |

| 14 | 58 | Santa Rosa-Petaluma, CA | 72 | 0.16% |

| 15 | 60 | Trenton-Princeton NJ | 71 | 0.16% |

| 16 | 61 | Portland-South Portland-Biddeford, ME | 70 | 0.16% |

| 17 | 62 | Albuquerque, NM | 68 | 0.15% |

| 18 | 64 | Reno-Sparks, NV | 62 | 0.14% |

| 19 | 65 | Santa Cruz-Watsonville, CA | 61 | 0.14% |

| 20 | 67 | Albany-Schenectady-Troy, NY | 60 | 0.14% |

| United States Total | 43,894 | |||

The pattern is similar when we look at shares of venture capital deals (see Table 9). Just two heartland metros crack the top 20: Madison, Wisconsin (fifth place with 0.29%) and Ann Arbor, Michigan (ninth with 0.26%).

Table 10: Share Of Venture Capital Investment For Heartland Metros

| HEARTLAND METRO RANK | OVERALL RANK | METRO | INVESTMENT (MILLIONS) | SHARE |

|---|---|---|---|---|

| 1 | 8 | Austin-Round Rock, TX | $11,787 | 1.93% |

| 2 | 9 | Chicago-Naperville-Joliet, IL-IN-WI | $11,779 | 1.93% |

| 3 | 15 | Minneapolis-St. Paul-Bloomington, MN-WI | $5,154 | 0.84% |

| 4 | 16 | Dallas-Fort Worth-Arlington, TX | $5,082 | 0.83% |

| 5 | 20 | Houston-Sugar Land-Baytown, TX | $3,262 | 0.53% |

| 6 | 21 | Columbus, OH | $2,921 | 0.48% |

| 7 | 28 | Nashville-Davidson-Murfreesboro-Franklin, TN | $1,935 | 0.32% |

| 8 | 32 | St. Louis, MO-IL | $1,532 | 0.25% |

| 9 | 34 | Detroit-Warren-Livonia, MI | $1,323 | 0.22% |

| 10 | 42 | Madison, WI | $876 | 0.14% |

| 11 | 44 | Indianapolis-Carmel, IN | $829 | 0.14% |

| 12 | 45 | Kansas City, MO-KS | $799 | 0.13% |

| 13 | 48 | Ann Arbor, MI | $721 | 0.12% |

| 14 | 49 | Cleveland-Elyria-Mentor, OH | $614 | 0.10% |

| 15 | 50 | Cincinnati-Middletown, OH-KY-IN | $583 | 0.10% |

| 16 | 54 | San Antonio, TX | $451 | 0.07% |

| 17 | 58 | Louisville/Jefferson County, KY-IN | $419 | 0.07% |

| 18 | 59 | Birmingham-Hoover, AL | $418 | 0.07% |

| 19 | 61 | Lincoln, NE | $343 | 0.06% |

| 20 | 63 | Columbia, MO | $318 | 0.05% |

| United States Total | $611,566 | |||

TABLE 11: SHARE OF VENTURE CAPITAL DEALS FOR HEARTLAND METROS

| HEARTLAND METRO RANK | OVERALL RANK | METRO | DEALS | SHARE |

|---|---|---|---|---|

| 1 | 7 | Austin-Round Rock, TX | 1,145 | 2.61% |

| 2 | 9 | Chicago-Naperville-Joliet, IL-IN-WI | 1,100 | 2.51% |

| 3 | 15 | Dallas-Fort Worth-Arlington, TX | 625 | 1.42% |

| 4 | 16 | Houston-Sugar Land-Baytown, TX | 465 | 1.06% |

| 5 | 17 | Minneapolis-St. Paul-Bloomington, MN-WI | 421 | 0.96% |

| 6 | 25 | Indianapolis-Carmel, IN | 256 | 0.58% |

| 7 | 26 | Nashville-Davidson-Murfreesboro-Franklin, TN | 247 | 0.56% |

| 8 | 31 | Detroit-Warren-Livonia, MI | 195 | 0.44% |

| 9 | 32 | St. Louis, MO-IL | 193 | 0.44% |

| 10 | 33 | Columbus, OH | 186 | 0.42% |

| 11 | 36 | Kansas City, MO-KS | 139 | 0.32% |

| 12 | 38 | Cleveland-Elyria-Mentor, OH | 131 | 0.30% |

| 13 | 40 | Madison, WI | 126 | 0.29% |

| 14 | 44 | Cincinnati-Middletown, OH-KY-IN | 120 | 0.27% |

| 15 | 45 | Ann Arbor, MI | 112 | 0.26% |

| 16 | 47 | San Antonio, TX | 94 | 0.21% |

| 17 | 48 | Louisville/Jefferson County, KY-IN | 90 | 0.21% |

| 18 | 50 | Birmingham-Hoover, AL | 88 | 0.20% |

| 19 | 54 | Milwaukee-Waukesha-West Allis, WI | 80 | 0.18% |

| 20 | 65 | Grand Rapids-Wyoming, MI | 61 | 0.14% |

| United States Total | 43,894 | |||

Even the leading heartland metros capture a relatively small share of venture capital deals and investments (see Tables 10 and 11).

- The top performers are Austin, Texas and Chicago, with roughly 2.5% of deals, followed by Dallas (1.42%) and Houston (1.06%).

- Three more have between 0.5% and 1%: Minneapolis-St. Paul (0.96%), Indianapolis (0.58%) and Nashville, Tennessee (0.56%).

- The remainder have less than half a percent: Detroit and St. Louis (with 0.44% each), Columbus, Ohio (0.42%), Kansas City, Missouri- Kansas (0.32%), Cleveland (0.30%), Madison, Wisconsin (0.29%), Cincinnati (0.27%), Ann Arbor, Michigan (0.26%), San Antonio, Texas and Louisville, Kentucky (both 0.21%), Birmingham, Alabama (0.20%), Milwaukee, Wisconsin (0.18%) and Grand Rapids, Michigan (0.14%).

FIGURE 10: PERCENTAGE POINT GROWTH IN SHARE OF VENTURE CAPITAL INVESTMENT

FIGURE 11: PERCENTAGE POINT GROWTH IN SHARE OF VENTURE CAPITAL DEALS

Changes in their shares of venture capital activity were miniscule for heartland metros. Only one posted an increase of even half a percentage point – Chicago, with 0.51% growth for venture capital deals – and most were significantly below that (see Tables 12 and 13 and Figures 10 and 11).

Table 12: Percentage Point Growth In Share

Of Venture Capital Investment For Heartland Metros

| HEARTLAND RANK | OVERALL RANK | METRO | CHANGE IN SHARE |

|---|---|---|---|

| 1 | 6 | Columbus, OH | 0.36% |

| 2 | 20 | Columbia, MO | 0.05% |

| 3 | 21 | Birmingham-Hoover, AL | 0.04% |

| 4 | 31 | Lincoln, NE | 0.03% |

| 5 | 34 | Springfield, MO | 0.02% |

| 6 | 37 | Midland, TX | 0.02% |

| 7 | 40 | Milwaukee-Waukesha-West Allis, WI | 0.02% |

| 8 | 45 | Grand Forks, ND-MN | 0.02% |

| 9 | 49 | Dayton, OH | 0.01% |

| 10 | 51 | Chattanooga, TN-GA | 0.01% |

| 11 | 53 | Omaha-Council Bluffs, NE-IA | 0.01% |

| 12 | 55 | Iowa City, IA | 0.01% |

| 13 | 59 | Des Moines-West Des Moines, IA | 0.01% |

| 14 | 61 | Joplin, MO | 0.01% |

| 15 | 62 | Fayetteville-Springdale-Rogers, AR-MO | 0.01% |

| 16 | 66 | Pine Bluff, AR | 0.01% |

| 17 | 67 | Elizabethtown, KY | 0.01% |

| 18 | 69 | Peoria, IL | 0.01% |

| 19 | 71 | Waterloo-Cedar Falls, IA | 0.01% |

| 20 | 73 | Oklahoma City, OK | 0.00% |

TABLE 13: PERCENTAGE POINT GROWTH IN SHARE OF VENTURE CAPITAL DEALS FOR HEARTLAND METROS

| HEARTLAND METRO RANK | OVERALL RANK | METRO | CHANGE IN SHARE |

|---|---|---|---|

| 1 | 5 | Chicago-Naperville-Joliet, IL-IN-WI | 0.515% |

| 2 | 9 | Austin-Round Rock, TX | 0.154% |

| 3 | 11 | Houston-Sugar Land-Baytown, TX | 0.127% |

| 4 | 27 | South Bend-Mishawaka, IN-MI | 0.052% |

| 5 | 30 | Grand Rapids-Wyoming, MI | 0.047% |

| 6 | 31 | Indianapolis-Carmel, IN | 0.045% |

| 7 | 36 | Birmingham-Hoover, AL | 0.040% |

| 8 | 38 | Detroit-Warren-Livonia, MI | 0.038% |

| 9 | 42 | Rochester, MN | 0.028% |

| 10 | 43 | Little Rock-North Little Rock-Conway, AR | 0.027% |

| 11 | 46 | Lincoln, NE | 0.026% |

| 12 | 49 | Fayetteville-Springdale-Rogers, AR-MO | 0.024% |

| 13 | 53 | Columbia, MO | 0.022% |

| 14 | 53 | Iowa City, IA | 0.022% |

| 15 | 55 | Omaha-Council Bluffs, NE-IA | 0.020% |

| 16 | 57 | Des Moines-West Des Moines, IA | 0.019% |

| 17 | 60 | Green Bay, WI | 0.018% |

| 18 | 64 | Battle Creek, MI | 0.016% |

| 19 | 64 | Lafayette, LA | 0.016% |

| 20 | 69 | Wichita, KS | 0.014% |

As noted earlier, only three metros across the entire nation significantly increased their shares of venture capital over the past decade (see Tables 14 and 15).

- New York City saw by far the largest gain, posting increases in both its share of venture capital investment (6.71%) and venture capital deals (3.64%).

- San Francisco takes second for growth in its share of venture capital investment (4.72%) but has seen a much slower rate of growth in venture capital deals (0.82%).

- Los Angeles takes second place for growth in venture capital deals (2.14%) and is third for growth of venture capital investment (1.48%).

- Strikingly, no other metro managed to grow its share of venture capital by even one percentage point (see Tables 14-17). Established tech hubs like Seattle (0.57%) and Boston (0.49%) registered about a half percentage point of growth in venture investment. For all the hype about its rise as a high-tech startup hub, Miami registered growth of just a tenth of a percent (0.09%) in venture capital investment.

TABLE 14: PERCENTAGE POINT GROWTH IN SHARE OF VENTURE CAPITAL INVESTMENT FOR LARGE METROS

| LARGE METRO RANK | OVERALL RANK | METRO | CHANGE IN SHARE |

|---|---|---|---|

| 1 | 1 | New York-Northern New Jersey-Long Island, NY-NJ-PA | 6.71% |

| 2 | 2 | San Francisco-Oakland-Fremont, CA | 4.72% |

| 3 | 3 | Los Angeles-Long Beach-Santa Ana, CA | 1.48% |

| 4 | 4 | Seattle-Tacoma-Bellevue, WA | 0.57% |

| 5 | 5 | Boston-Cambridge-Quincy, MA-NH | 0.49% |

| 6 | 6 | Columbus, OH | 0.36% |

| 7 | 7 | Phoenix-Mesa-Scottsdale, AZ | 0.16% |

| 8 | 8 | Sacramento-Arden-Arcade-Roseville, CA | 0.15% |

| 9 | 9 | Salt Lake City, UT | 0.14% |

| 10 | 16 | Miami-Fort Lauderdale-Pompano Beach, FL | 0.09% |

| 11 | 21 | Birmingham-Hoover, AL | 0.04% |

| 12 | 23 | Las Vegas-Paradise, NV | 0.04% |

| 13 | 24 | Riverside-San Bernardino-Ontario, CA | 0.04% |

| 14 | 33 | Fresno, CA | 0.02% |

| 15 | 35 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | 0.02% |

| 16 | 36 | Virginia Beach-Norfolk-Newport News, VA-NC | 0.02% |

| 17 | 40 | Milwaukee-Waukesha-West Allis, WI | 0.02% |

| 18 | 52 | Buffalo-Niagara Falls, NY | 0.01% |

| 19 | 65 | Jacksonville, FL | 0.01% |

| 20 | 73 | Oklahoma City, OK | 0.00% |

Table 15: Percentage Point Growth In Share Of Venture Capital Deals For Large Metros

| LARGE METRO RANK | OVERALL RANK | METRO | CHANGE IN SHARE |

|---|---|---|---|

| 1 | 1 | New York-Northern New Jersey-Long Island, NY-NJ-PA | 3.64% |

| 2 | 2 | Los Angeles-Long Beach-Santa Ana, CA | 2.14% |

| 3 | 3 | San Francisco-Oakland-Fremont, CA | 0.82% |

| 4 | 4 | Miami-Fort Lauderdale-Pompano Beach, FL | 0.65% |

| 5 | 5 | Chicago-Naperville-Joliet, IL-IN-WI | 0.51% |

| 6 | 6 | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD | 0.51% |

| 7 | 7 | Denver-Aurora, CO | 0.33% |

| 8 | 9 | Austin-Round Rock, TX | 0.15% |

| 9 | 10 | Phoenix-Mesa-Scottsdale, AZ | 0.14% |

| 10 | 11 | Houston-Sugar Land-Baytown, TX | 0.13% |

| 11 | 12 | Charlotte-Gastonia-Concord, NC-SC | 0.11% |

| 12 | 13 | Las Vegas-Paradise, NV | 0.10% |

| 13 | 15 | Richmond, VA | 0.09% |

| 14 | 16 | Tampa-St. Petersburg-Clearwater, FL | 0.08% |

| 15 | 17 | Buffalo-Niagara Falls, NY | 0.08% |

| 16 | 18 | Riverside-San Bernardino-Ontario, CA | 0.08% |

| 17 | 19 | Sacramento-Arden-Arcade-Roseville, CA | 0.07% |

| 18 | 21 | Virginia Beach-Norfolk-Newport News, VA-NC | 0.07% |

| 19 | 30 | Grand Rapids-Wyoming, MI | 0.05% |

| 20 | 31 | Indianapolis-Carmel, IN | 0.05% |

Table 16: Percentage Point Growth

In Share Of Venture Capital Investment For Smaller Metros

| SMALLER METRO RANK | OVERALL RANK | METRO | CHANGE IN SHARE |

|---|---|---|---|

| 1 | 10 | Provo-Orem, UT | 0.14% |

| 2 | 11 | Albany-Schenectady-Troy, NY | 0.12% |

| 3 | 12 | Santa Cruz-Watsonville, CA | 0.12% |

| 4 | 13 | Reno-Sparks, NV | 0.12% |

| 5 | 14 | Dover, DE | 0.11% |

| 6 | 15 | Bridgeport-Stamford-Norwalk, CT | 0.09% |

| 7 | 17 | Carson City, NV | 0.07% |

| 8 | 18 | Boise City-Nampa, ID | 0.06% |

| 9 | 19 | New Haven-Milford, CT | 0.05% |

| 10 | 20 | Columbia, MO | 0.05% |

| 11 | 22 | Harrisonburg, VA | 0.04% |

| 12 | 25 | Sarasota-Bradenton-Venice, FL | 0.03% |

| 13 | 26 | Burlington, NC | 0.03% |

| 14 | 27 | Oxnard-Thousand Oaks-Ventura, CA | 0.03% |

| 15 | 28 | Burlington-South Burlington, VT | 0.03% |

| 16 | 29 | Santa Fe, NM | 0.03% |

| 17 | 30 | Huntington-Ashland, WV-KY-OH | 0.03% |

| 18 | 31 | Lincoln, NE | 0.03% |

| 19 | 32 | Naples-Marco Island, FL | 0.03% |

| 20 | 34 | Springfield, MO | 0.02% |

Table 17: Percentage Point Growth

In Share Of Venture Capital Deals For Smaller Metros

| SMALLER METRO RANK | OVERALL RANK | METRO | CHANGE IN SHARE |

|---|---|---|---|

| 1 | 8 | Dover, DE | 0.261% |

| 2 | 14 | Provo-Orem, UT | 0.093% |

| 3 | 20 | Albany-Schenectady-Troy, NY | 0.068% |

| 4 | 22 | Bremerton-Silverdale, WA | 0.061% |

| 5 | 23 | San Luis Obispo-Paso Robles, CA | 0.061% |

| 6 | 24 | Charlottesville, VA | 0.061% |

| 7 | 25 | Boise City-Nampa, ID | 0.055% |

| 8 | 26 | Asheville, NC | 0.052% |

| 9 | 27 | South Bend-Mishawaka, IN-MI | 0.052% |

| 10 | 28 | Naples-Marco Island, FL | 0.051% |

| 11 | 29 | Cheyenne, WY | 0.050% |

| 12 | 32 | Oxnard-Thousand Oaks-Ventura, CA | 0.045% |

| 13 | 33 | Spokane, WA | 0.043% |

| 14 | 33 | Winston-Salem, NC | 0.043% |

| 15 | 35 | Palm Bay-Melbourne-Titusville, FL | 0.042% |

| 16 | 37 | Fort Collins-Loveland, CO | 0.039% |

| 17 | 39 | Anchorage, AK | 0.035% |

| 18 | 40 | Reno-Sparks, NV | 0.033% |

| 19 | 41 | Coeur d’Alene, ID | 0.030% |

| 20 | 42 | Rochester, MN | 0.028% |

The Big Shifts

The most significant trend to emerge from our data and analysis is that the overall increase in venture capital over the past decade has spurred the growth of new startup ecosystems. While venture capital remains concentrated in established tech hubs, functional startup ecosystems are emerging in heartland communities and across America.

Within this overall trend there are a series of more specific patterns:

- Venture capital investment in the heartland has grown significantly over the past decade, surging by nearly 400% from $15 billion in 2009-11 to $55 billion in 2019-21.

- The heartland is now home to a number of significant startup ecosystems. Two heartland metros –Austin, Texas and Chicago – rank among the nation’s leading startup ecosystems, behind only the San Francisco Bay Area, Boston- Cambridge, Los Angeles, San Diego and Seattle. Four other heartland metros – Minneapolis-St. Paul, Dallas, Houston and Columbus, Ohio – rank among the nation’s top 20 centers for venture investment.

- Four heartland metros rank among the top 20 large metros on per capita venture investment: Austin, Texas, Minneapolis-St. Paul, Columbus, Ohio, Chicago and Nashville, Tennessee. A ranking from early 2023 placed Nashville, Tennessee fifth nationally in venture investment behind only the Bay Area, New York City, Boston, and Los Angeles.17

- The startup ecosystems of some heartland metros are comparable in size to those of leading tech hubs in the mid-1990s. Adjusting for inflation, eleven metros, including the heartland metros of Austin, Texas and Chicago, have levels of venture capital investment that are comparable to Silicon Valley back in 1995; 18 metros, including four heartland metros, have as much venture capital investment as Boston did; and 26, including six heartland metros, have as much as Washington, D.C. did in 1995.

- An even larger number of heartland metros have registered significant growth in venture capital investment. Columbus, Ohio, Birmingham, Alabama, Milwaukee, and Oklahoma City all register in the top 20 large metros on venture capital investment growth, while Grand Rapids, Michigan and Indianapolis rank among the top 20 large metros for growth in venture capital deals.

- A range of smaller heartland communities have posted substantial growth in venture capital investment. As we have seen, venture investment in Grand Forks, North Dakota grew by more than 60,000% – the second fastest rate of growth of any metro in the country. Four heartland metros saw venture capital investment surge by more than 5,000%. Another seven saw gains of between 2,000% and 4,000%. And 10 more saw growth of between 1,000 and 2,000%.

- The heartland’s college towns are a critical part of the equation. The region’s largest startup hubs are all homes to major research universities: Austin, Texas (with the University of Texas at Austin), Chicago (University of Chicago and Northwestern University), Columbus, Ohio (The Ohio State University), Minneapolis-St. Paul (University of Minnesota) and Nashville, Tennessee (Vanderbilt University). More fledgling startup ecosystems have emerged across the region’s classic college towns like Ann Arbor, Michigan (home to the University of Michigan), Madison, Wisconsin (University of Wisconsin), Lincoln, Nebraska (University of Nebraska), Columbia, Missouri (University of Missouri), South Bend, Indiana (University of Notre Dame), Grand Forks, North Dakota (University of North Dakota) and Fayetteville, Arkansas (University of Arkansas), to name just a few.

- Overall, nearly three quarters of heartland metros receive venture capital investment.

- Despite the tremendous growth and spread of venture capital and startup ecosystems across the heartland, the overall landscape of venture capital investment remains spiky. The heartland accounts for less than 10% of the nation’s investment and just 16% of deals, while making up more than a quarter of its population and economic output. The San Francisco Bay Area accounts for significantly more venture capital investment than the entire heartland. Just three metros – New York City, Los Angeles, and San Francisco – saw appreciable gains in their share of the nation’s venture capital dollars and deals over the past decade.

A New Model Of Industry- Transforming Innovation

The past decade has been good for the development of innovation in the heartland and bodes well for the future of the region and the nation. The challenge is to accelerate it while forging a new model of innovation that links it to broader industrial transformation.

Focus On Entrepreneurs And Ecosystems

The first step is to strengthen startup ecosystems across the region. Venture capitalists Brad Feld and Ian Hathaway have outlined the key principles for doing so.18

As they describe them, startup communities are complex adaptive systems that emerge organically and depend on an intricate balance of entrepreneurs, venture capitalists, and research universities, among other organizations and institutions. There is no simple recipe that can generate a successful startup ecosystem, and if one does come into being, the cadence and extent of its growth tends to be unpredictable. But Feld and Hathaway outline several principles that communities can use to develop and strengthen their startup ecosystems. The best approach, which is to:

- Identify successful entrepreneurs and entrepreneurial enterprises.

- Allow entrepreneurs to lead.

- Establish networks that connect fledgling entrepreneurs with more experienced ones, who can act as mentors.

- Ensure that the emerging startup ecosystem is inclusive of all who desire to participate.

- Build broader systems and ecologies to support entrepreneurial talent.

- Use entrepreneurs to identify missing elements of the system.

- Track progress over time and revise as required.

It is important to distinguish entrepreneurial talent (the ability to build and scale new firms) from technological talent (the ability to develop technological innovations). They are far from the same thing. In fact, the key to successful startups and startup ecosystems is a plentiful supply of serial entrepreneurs – people who know how to recognize opportunity, manage risk, and build organizational capability. Successful entrepreneurs frequently become angel investors and venture capitalists as well.

Develop Entrepreneurial Talent

Even if they lack this entrepreneurial talent, regions can build it up in various ways. One is by working with existing technologists, entrepreneurs and startups to build and enhance their entrepreneurial capabilities. Initiatives like the Idea Accelerator program, the Builders + Backers initiative powered by Heartland Forward, and the National Science Foundation’s Innovation Corps (or I-Corps) work with entrepreneurs to develop the business skills, resources, and networks that they need to get their business ideas and start-ups off the ground.19 The Creative Destruction Lab at the University of Toronto’s Rotman School of Management pairs fledgling entrepreneurs with teams of MBA students and convenes seasoned entrepreneurs to meet with them every few months to review their progress, revise and reset their priorities, and otherwise help scale their startups.20

Cities and regions can also tap into remote sources of entrepreneurial talent. Most have diasporas of people who grew up or went to college there before moving to leading tech hubs. Leaders can tap these people for advice, investments, and other kinds of support, and even lure some of them back.

Entrepreneurs often bemoan the dearth of early- stage funding. Policymakers sometimes respond by setting up government-backed programs to provide it. These capital programs, if they are well-crafted, respond to market signals, and to the extent that they are insulated from politics, can play a supportive role. But a large body of research has shown that they can be ineffective or even counter-productive when political or geographic conditions interfere.21 The lack of local venture capital is less a problem in-and-of-itself, and more a symptom of a lack of entrepreneurial talent and/or an underdeveloped entrepreneurial ecosystem.

Turn Universities Into Ecosystem Anchors

If entrepreneurs and entrepreneurial talent are central to the success of startups, research universities are their most important institutional anchors. In addition to their production of cutting-edge research that can be exploited commercially, research universities are powerful magnets for scientific, technical, and entrepreneurial talent.

The heartland is home to 38.8% of the nation’s leading-edge (so-called R1) research universities (with 40 of 103 such institutions). Overall, heartland-based universities conducted more than $30 billion in higher education R&D in 2021, more than a third (33.7%) of the nation’s total.22

But most heartland universities lag on the transfer of their research to industry. According to a 2022 Heartland Forward analysis, only five heartland universities ranked among the nation’s top 20 research institutions for technology transfer and commercialization: University of Minnesota (10th), Purdue University (11th), Northwestern University (13th), University of Michigan (16th), and the University of Texas at Austin (20th).

Several other heartland universities cracked the top 50: University of Chicago (24th), The Ohio State University (32nd), University of Houston (36th), University of Wisconsin-Madison (30th), Case Western University (39th), University of Kansas (41st) and Iowa State University (43rd).

By way of comparison, Carnegie Mellon ranked first; Stanford, 4th; Harvard, 5th; and MIT eleventh on this score.23

It is almost impossible to think of a leading startup hub, or a fledgling one for that matter, that is not anchored by a significant research university. Under the leadership of its legendary provost Frederick Terman, Stanford University took the initial steps that catalyzed Silicon Valley back in the 1950s, focusing on building steeples of excellence in electrical engineering. Terman also played the key role in creating the Stanford Research Park adjacent to the university to, which housed commercially oriented research and companies. He encouraged promising graduates like William Hewlett and David Packard to form early startup companies to help build up the local economy. Hewlet Packard established its headquarters in Research Park in 1956.

Similarly, there would be no high-tech complex in Boston without MIT and Harvard. When the region’s textile and footwear industries declined after World War II, retired general Georges Doriot, a faculty member at Harvard Business School, led the effort to create the world’s first organized venture capital fund, American Research and Development (ARD), to commercialize the new technology coming out of MIT and other universities.

Pittsburgh followed a similar path decades later when its steel and other heavy industries declined. Carnegie Mellon President Richard Cyert built up the cutting-edge areas of computer science, software engineering, artificial intelligence and robotics, and he invested in a series of technology transfer and entrepreneurial support initiatives.

But perhaps the best example of how a research university can catalyze a high-tech ecosystem comes from the heartland itself. In the late 1970s, the University of Texas at Austin recruited George Kozmetsky to become dean of its business school. Kozmetzky brought the knowledge he had gained as a co-founder of Teledyne, a tech-based startup in California backed by the legendary venture capitalist Arthur Rock, and before that as a young professor at Carnegie Mellon. To focus this effort, he created the IC2 Institute, the high-tech think tank that played a pivotal role, if not the pivotal role, in the development of Austin’s high-tech ecosystem, identifying key strategies and organizing the region’s business, political and academic leaders around them. IC2 helped to organize and lead the city’s efforts to land large federal installations, such as MCC and Sematech, recruit established high-tech companies and talent to the region, and develop its startup ecosystem.

Heartland community and university leaders can learn from these strategies and apply them to college towns across the region. To this end, universities must make technology transfer and commercialization and startup generation part of their core missions. State and local governments should consider partnering with universities and contributing funding to these efforts. The heartland would also benefit from creating a network or consortium of leading universities to share ideas and identify best practices along these lines.

Build Up College Towns

The region needs to think more strategically about college towns as well. They are not just places for kids to get an education or for students, residents and alums to enjoy big football games on fall Saturdays. They can and should act as talent magnets and anchors of the innovation economy.

Just as young techies tend to prefer startups over established companies because of the flexibility and excitement they offer, they are attracted to college towns because they are smaller and less daunting than big cities like New York City and San Francisco.24 Palo Alto, California, Cambridge, Massachusetts, Boulder, Colorado and Austin, Texas are places that young talent want to stay in and start their careers, either joining startups or creating ones of their own.

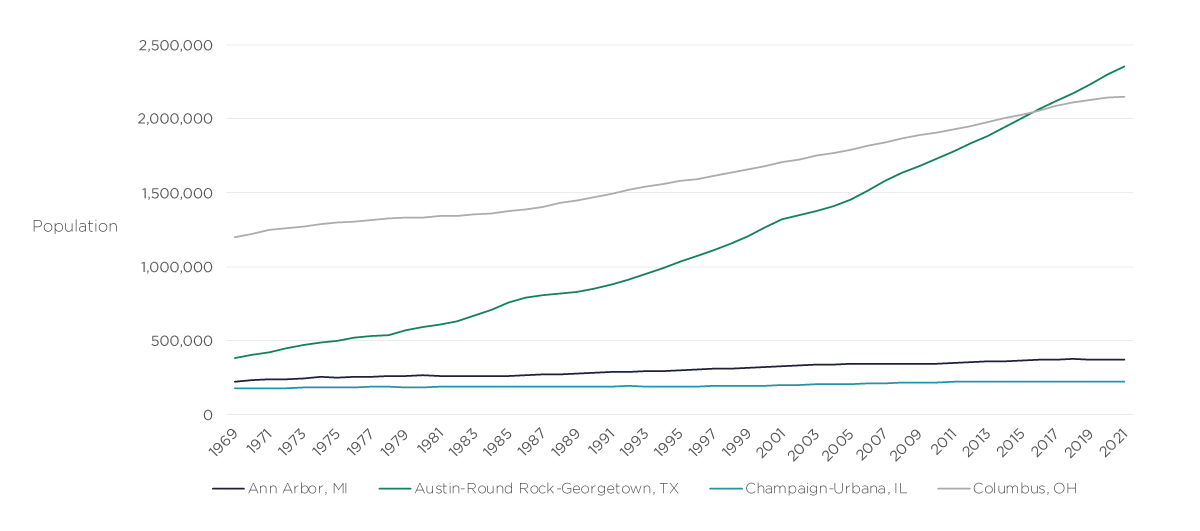

FIGURE 12: GROWTH IN POPULATION: SELECTED HEARTLAND COLLEGE TOWNS, 1969–2021

Austin, Texas, Nashville, Tennessee and Columbus, Ohio are already magnets for tech talent. Chicago and the Twin Cities of Minneapolis-St. Paul attract talent to a broader base of jobs and industries. But most heartland college towns act as “processing centers” for talent.25 They attract students, build their education and skills, and then export them when they graduate. That needs to change.

The benefits of college towns redound to whole regions. When their flywheels of startup innovation start in motion, they generate significant spillover growth. Palo Alto, California fuelled the whole Bay Area’s evolution into the world’s leading high-tech complex. MIT and Harvard powered the rise of greater Boston’s high-tech and biomedical complex. The growth of startups around Boulder, Colorado and the University of Colorado eventually helped to shape Denver’s rise as a high-tech hub.

Consider the very different growth trajectories of four leading heartland college towns: Austin, Texas, Ann Arbor, Michigan, Champaign-Urbana, Illinois and Columbus, Ohio (see Figure 11). In 1970, three of these metros – Austin, Ann Arbor and Champaign-Urbana – were relatively small. Champaign-Urbana was home to about 180,000 people. Ann Arbor’s population was roughly 230,000 and Austin’s was about 400,000. Only Columbus was home to more than a million people (1.22 million).

Since then, their growth has diverged widely. Austin’s population grew to more than a million by the mid- 1990s, to 1.5 million by the mid-2000s, and nearly 2.3 million in 2020, an overall growth rate of 472%. Even though Columbus started out much larger, its population still exploded to 2.1 million people by 2020 – an overall growth rate of about 75%. Over the same period, Ann Arbor’s population grew to just 370,000, a growth rate of 59%. It is still not the size that Austin was in 1970. Champaign-Urbana grew even slower, at a rate of 24% over this period.

The differential is even bigger for total income, a basic barometer of economic health. In 1970, Champaign-Urbana’s total personal income was $726 million; Columbus’ was $5 billion; Ann Arbor’s was $7.8 billion; and Austin’s was $9.5 billion. By 2021, Columbus’ total income had ballooned to $129 billion and Austin’s to $168 billion – the latter nearly seven times Ann Arbor’s $25.4 billion and roughly eleven times Champaign-Urbana’s $12.3 billion. Today, Columbus and Austin rank among the nation’s leading tech hubs, while Ann Arbor and Champaign-Urbana remain lovely college towns with fledgling startup ecosystems.

The heartland has dozens of college towns that could evolve into mini-Austins. There is enormous potential in enabling them to scale into bigger, more effective talent magnets and innovation catalysts.

Pave the Way for Industry-Transforming Innovation

The heartland can forge a new and potentially more transformative model for innovation. As the center for American manufacturing, it can do more than just invent new technologies and spin them out as startups. It has even more to gain from applying its innovative capacity to improve the competitiveness of its key manufacturing industries.

In the past, regions, states or nations have followed one of two paths for technology-based economic development.26 The first is “shifting”— essentially applying new technologies to generate wholly new industries, often in new geographic regions. That was the basic growth model followed by the United States over the past half century. Faced with escalating global competition and the decline of older industries like steel, autos, chemicals, and consumer electronics, it pivoted toward semiconductors, computers, software, biotechnology, the Internet, and social media. Shifting is also the path adopted by older U.S. regions seeking to cope with the decline of their incumbent industries, like Boston and Pittsburgh.27

The second path is “deepening,” the application of technology to incrementally improve existing industries. This is the path that Germany, Japan and Korea have taken by upgrading their steel, auto, chemical, consumer electronics and related industries.

The heartland has a unique opportunity to join both paths – to shift and deepen simultaneously, and in so doing forge a new and more holistic model for innovation and economic development.

The heartland remains the nation’s industrial center of gravity, despite the legacy of deindustrialization that tragically hollowed out so many of its older industrial communities. It is home to more than half (50.5%) of the nation’s private sector manufacturing employment, 6.5 million of America’s 12.8 million manufacturing workers. Its manufacturing productivity is about 7.5% better than that of the nation as a whole. Its economic output in 2022 was $16.5 trillion, equivalent to the world’s third largest economy.28

Over the past several decades, the region’s industrial geography has shifted. Originally anchored in and around the Great Lakes states of Michigan, Ohio, Illinois, and Indiana, it has expanded southward. Heartland metros like Nashville and Knoxville, Tennessee; Birmingham and Huntsville, Alabama; Jackson, Mississippi; Kansas City, Missouri; Indianapolis, Evansville, South Bend and Fort Wayne, Indiana; and Columbus, Ohio have joined places like Detroit, Cleveland, and Dayton and Toledo, Ohio as the nation’s major automotive industry clusters.29 Michigan, Ohio, Indiana, Kentucky, Tennessee, and Alabama comprise the nation’s six leading centers for automotive production. Transformative investments in technology-based manufacturing are being made across the region. Those states and Texas all number among the national leaders for new investments in electric vehicle and battery manufacturing.30 On top of that, some of most advanced logistics and distribution capabilities in the nation are located in Northwest Arkansas, home to Walmart and J.B. Hunt, and in Memphis, Tennessee, home to FedEx.

Many, if not most, of the heartland’s leading industrial clusters are close to major universities and college towns. Proximity to research universities has playeda key role in attracting some of the largest advanced manufacturers to the region. Elon Musk located his Tesla Gigafactory outside Austin, and Intel sited its massive semiconductor fabrication complex near Columbus, Ohio.31

Technological capabilities often span different regions and sometimes cross state lines as well, creating considerable opportunities for cross regional collaboration. A good example of this is the “412 Innovation Corridor,” which joins the capabilities of two heartland communities, Northwest Arkansas and Tulsa.32 Northwest Arkansas is the home of the University of Arkansas as well as industry leaders like Walmart and J.B. Hunt Transport Services. Similarly, the Tulsa region is home to a major aerospace cluster and Oklahoma State University, that hosts the Unmanned Systems Research Institute, the first in the country to focus on aerial drones. Northwest Arkansas has bolstered its ability to attract and retain talent by investing in outdoor recreation with its nationally recognized network of cycling trails, and in arts and culture, including the world class Crystal Bridges Museum of American Art. Even before the pandemic, Tulsa developed a leading-edge effort to attract remote workers, Tulsa Remote, and built up what is now arguably the nation’s leading talent- attraction apparatus. In recent years, efforts such as Tulsa Innovation Labs have been started in a major effort to build a resilient innovation economy in high- tech clusters. Additional efforts run the gamut from talent initiatives, such as InTulsa, and venture capital funds such as Atento Capital, to investments in arts and culture such as the Woody Guthrie Museum, which now also houses the Bob Dylan archives, and its award-winning open space, The Gathering Place.33 More recently, the two regions invested in a joint office of Endeavor, the world’s leading entrepreneurial assistance and catalyst organization, to leverage their joint capabilities and attract federal funding as a leading cluster for advanced logistics and mobility.

The capabilities are all there: What is required is greater alignment across key business, academic, political, and civic leaders.

Tap into New Federal Initiatives and Funding

The federal government’s move to “place-based industrial policy” can help to leverage and accelerate this shift.34 Initiatives like the Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA), and CHIPS and Science Act are providing nearly $2 trillion to improve America’s competitive position in key industries, reshore its supplier base, achieve more balanced growth and create higher paying jobs.35 A sizeable chunk of this effort aims to bolster critical sectors like semiconductors, electric batteries, mobility and logistics by marrying advanced R&D at research universities to regionally based industrial clusters. These programs provide resources that enable local communities to further develop their innovative and productive capabilities, attract and mobilize talent, and create good, high-paying jobs, according to a recent Heartland Forward report.36

Sponsored by the Economic Development Administration of the Department of Commerce, the federal Tech Hubs initiative is poised to provide substantial investments in tech clusters across the country. 379 regions applied for consideration under its original phase 1 awards in the summer of 2023. In October, the administration designated 31 winning regions that will compete for $500 million in funding. Heartland communities received 12 of these awards. Many have a strong focus on transformative technology geared to actually making things, such as advanced semiconductor manufacturing in North Central Texas and Southern Oklahoma, polymers and advanced materials manufacturing in Akron, critical minerals processing to provide the materials for battery technology in Missouri, and autonomous systems in Tulsa.37

The Heartland Is Key to America’s Future

The massive growth of venture capital over the past decade has fueled the growth of viable startup ecosystems across the heartland, including some that are already comparable to what Silicon Valley and Boston were a generation ago. Fledgling ecosystems are emerging in college towns and smaller communities across the region, as well.