Note to reader: Over the next several weeks, Heartland Forward will be analyzing the types of businesses and races of business owners that received Paycheck Protection Program (PPP) loans through June 30, 2020.

You can preview the visualizations referenced below here:

(For mobile viewers, we recommend landscape orientation.)

Many retail and other service1 businesses were among those adversely impacted by social distancing restrictions because the working conditions require workers and customers to be near one another. With the notable exception of specific subsectors that were declared to be “essential workers” (such as grocery stores), many retail and other service facilities were closed during the economic shutdown to prevent the spread of COVID-19.

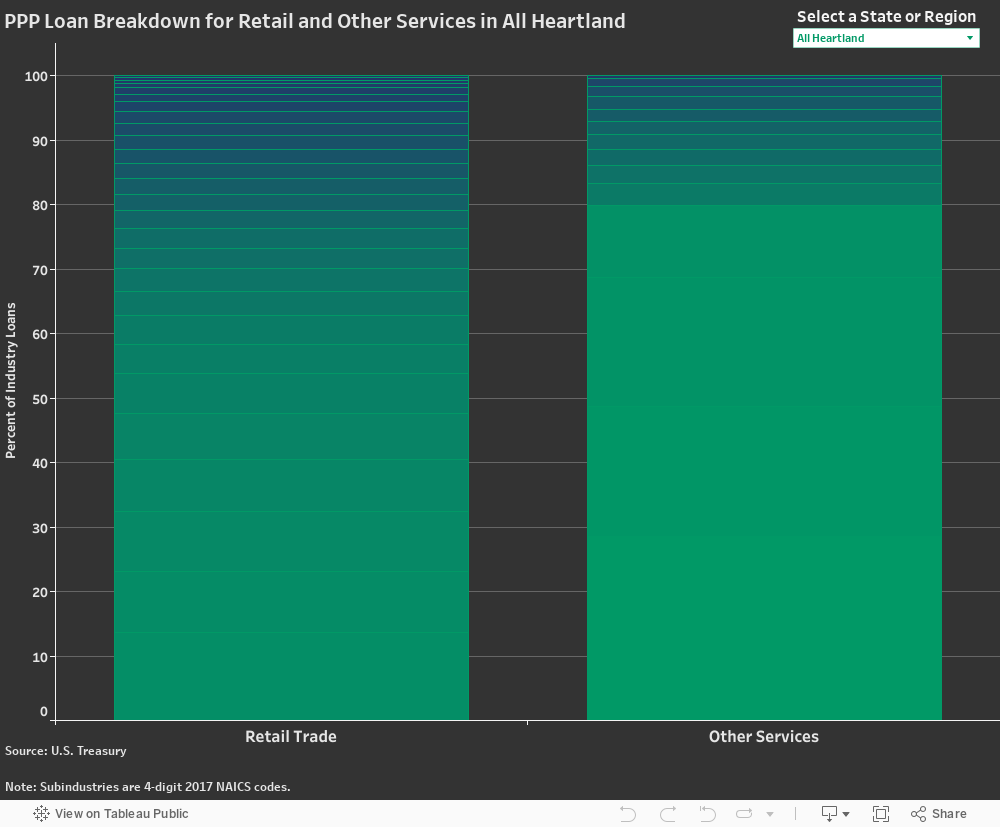

The first chart above shows the distribution of PPP loans in each industry. Across half the states in the Heartland2, more than 50 percent of the loans given to retail businesses were in the following six sectors: other miscellaneous retail, gas stations, auto dealers, grocers, health and personal care stores (i.e., drug stores), and clothing stores. In the other 10 states, some combination of these and building materials, auto parts, sporting and hobby goods stores, and beer, wine and liquor stores comprised over 50 percent of the PPP loans. For Other Services, roughly 80 percent of all loans in all 20 states went to the same four sectors: personal care services, auto repair and maintenance, religious organizations, and other personal services.3

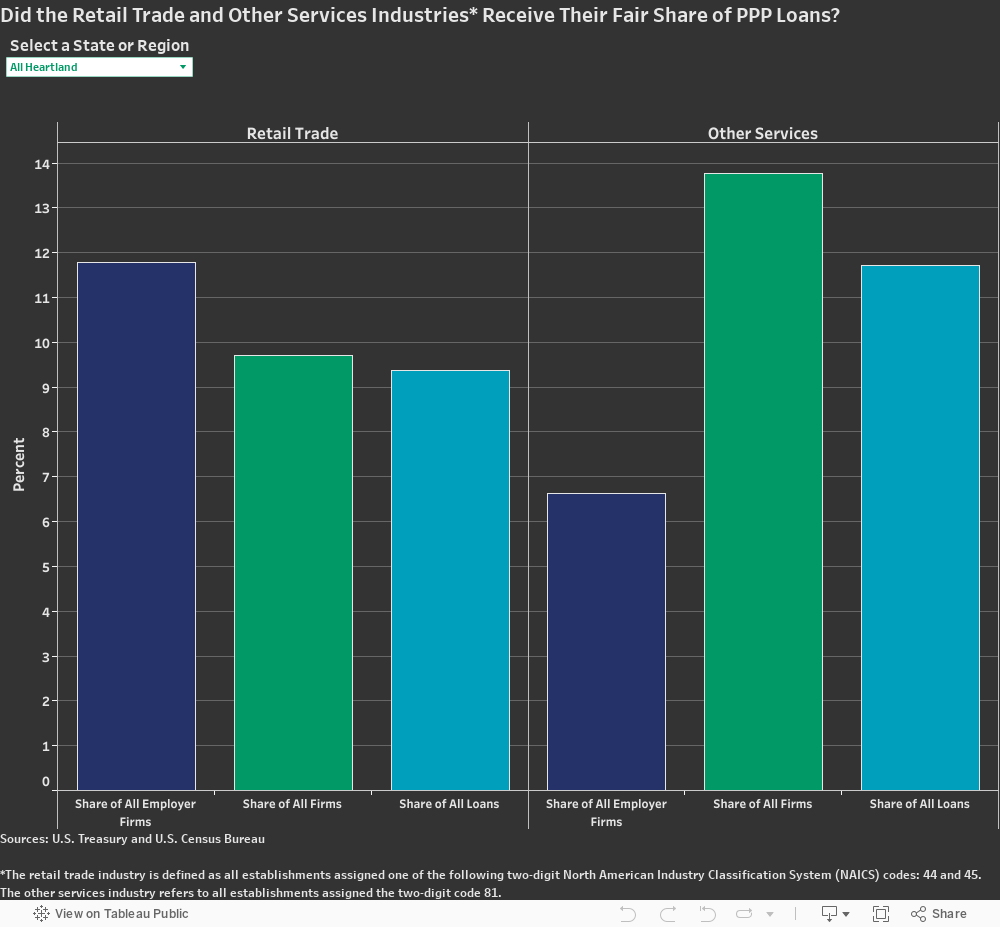

The second chart provides a comparison between the share of firms and the share of PPP loans granted in each industry. The first two columns in each chart represent the benchmark values: share of employer firms (i.e. firms that have employees beyond the firm owners) and share of all firms (which includes non-employer firms such as sole proprietors, contract workers and other self-employed individuals), respectively. When the industry’s share of all firms exceeds that of all employer firms, one can conclude that the industry has an outsized number of non-employer firms relative to other industries. The third column presents the share of loans going to retail and other service businesses. If the right-most column for an industry is higher than those to the left, then this indicates that the industry received a greater share of loans than one would expect based on the industry’s share of firms. If the share of loans is less than one percentage point higher or lower than the share of all employer firms or all firms, we consider these values to be equal.

Several observations:

• In all but two states (South Dakota and Wisconsin), the share of all employer firms in retail was greater than the share of all firms, suggesting that retail is more dense in employer firms than other industries.

• Minnesota, Nebraska and North Dakota had roughly equal shares of all employer firms and all firms.

• In all states, retail firms received a lesser share of PPP loans than their share of all employer firms.

• In five states (Alabama, Louisiana, Michigan, Mississippi and Tennessee), the share of PPP loans to retail businesses was at least one percentage point greater than the share of all firms in retail.

• In an additional five states (Arkansas, Illinois, Kentucky, Ohio and Texas), the share of PPP loans to retail businesses was roughly equal to the share of all firms.

• In all states, businesses in other services are more likely to be non-employers than in other industries. That is, the share of all firms is greater than the share of all employer firms.

• Five states (Kansas, Minnesota, Ohio, South Dakota and Wisconsin) have shares of PPP loans to other services greater than or equal to the share of all firms.

Payroll Protection Program (PPP) represents a unique stimulus program designed to encourage businesses to maintain payroll levels despite pandemic-related interruptions by authorizing local financial institutions to extend potentially forgivable loans at favorable terms. The program provided loans with an one-percent interest rate to qualifying businesses, though the loan would be forgiven if certain requirements were met by the business.4

While designed for expediency, the PPP sought to leverage existing financial institutions to distribute the loans rather than create tedious qualification rules and bureaucracy, which would have required both time and resources. However, expediency is not without cost – specifically, leveraging existing financial institutions may limit access to the PPP for small and non-employer business owners.

So, what does all this mean? Whether retail and other service businesses received their fair share of PPP loans largely depends on which state in the Heartland the businesses were located. Regardless, preserving retail and other service jobs during these unprecedented times is paramount to ensuring that local economies in general persist. Retail and other service jobs employ local workers and provide essential goods and services for local residents. The presence of retail and other services often makes communities livable.

Congress and the Trump administration need to reach an agreement on extending economic and financial aid to those firms and individuals most impacted by COVID-19. Another round of PPP loans should be a major piece of the legislation as retailers and other services are the core of many economies which provide jobs and generate sales tax revenue to support government services. The Heartland cannot afford to lose as single job that could be created by retail and other service businesses.

Below is the schedule of posts in this series:

• Week 1: Black and Hispanic Business Owners

• Week 2: American Indian, Pacific Islander and Asian Owned Businesses

• Week 3: Loan Recipients by Gender

• Week 4: Accommodations and Food Services & Arts, Entertainment, Recreation Businesses

• Week 5: Manufacturing

• Week 6: Retail & Other Services

Data Notes

Data on Payroll Protection Program loans are from the U.S. Treasury. These are loan-level data based on individual loan applications. We aggregated loan-level data to the state level in order to capture the state-level distribution of loans across industries.

Data on industry of employer firms are from the U.S. Census Bureau’s 2017 Annual Business Survey.

Data on owners of all firms (both employers and non-employers) are from the U.S. Census Bureau’s 2012 Survey of Business Owners. Use of these data are necessary due to the lack of publicly available information on non-employer firms from the 2017 Annual Business Survey.

ENDNOTES

- Retail businesses are categorized by the 4-digit North American Industrial Classification System (NAICS) codes starting with 44 and 45. Retail trade includes the following subsectors: automobile dealers; other motor vehicle dealers; automotive parts, accessories and tire stores; furniture stores; home furnishings stores (e.g., flooring and window treatments); electronics and appliance stores; building material and supplies; lawn and garden equipment stores; grocery stores; specialty food stores; beer, wine and liquor stores; health and personal care stores (e.g., pharmacies, cosmetics and optical goods stores); gasoline stores; clothing stores; shoes, jewelry and accessories stores; sporting goods, hobby and musical instrument stores; book stores and news dealers; general merchandise stores; florists; office supply, stationery and gift stores; used merchandise stores; other miscellaneous store retailers (such as pet supplies, art dealers, manufactured home dealers); and nonstore retailers (like electronic shopping and mail-order houses, vending machine operators and direct selling establishments).

Similarly, other services businesses are categorized by the 4-digit NAICS codes starting with 81; services covered include: automotive repair and maintenance; electronic, commercial and industrial, and personal and household goods repair and maintenance; personal care services (e.g., barbers, nail salons); death care services; drycleaning and laundry services; other personal services (such as pet care, photofinishing and parking services); religious organizations; grantmaking services; social advocacy organizations; civic and social organizations; business, professional, labor and political organizations; and private households.

- The Heartland region consists of these states: Alabama, Arkansas, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Michigan, Minnesota, Mississippi, Missouri, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Tennessee, Texas and Wisconsin.

- Each subsector has a unique color that is consistent across states. The Heartland possesses data for all subsectors, and the ranking of subsectors for the region determines the color scheme used across the states. By hovering over a particular band, you can identify the sector, as well as the number and share of loans of received.

- Complete details about the SBA’s Payroll Protection Program, including qualifying businesses and loan forgiveness criteria, can be found here: https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/paycheck-protection-program