EXECUTIVE SUMMARY

As the dominant economic geography of America, metropolitan statistical areas largely determine our success as a nation.

These groups of counties with a large central core account for 87.5 percent of jobs, 90.3 percent of wages and 88.3 percent of Gross Domestic Product (GDP). Further, metropolitan statistical areas account for the bulk of innovation such as research and development and patenting activity. Understanding the mechanisms underpinning the growth of top-performing metropolitan areas, and sharing best practices, could assist other communities to boost their economic fortunes. The Most Dynamic Metropolitan Index, ranking 375 metropolitan areas, seeks to provide an objective measure of communities’ economic vibrancy where the lion’s share of Americans work and live.

Our Most Dynamic Metropolitan Index and the analysis in this report provide objective insight into the communities providing economic opportunity for their residents, separating high performers from the low. Most Dynamic Metropolitans provides fact-based metrics on near-term and medium-term performance and prospects for long-term growth. The index allows economic development officials the ability to monitor their metro’s vivacity relative to others on a national basis or within their region and state. We also look through the lens of the Heartland—the 20 states in the middle of the nation—to discern its performance and understand practices that can boost economic prospects.

While international and national economic and geopolitical factors can influence growth patterns, the index provides an objective measure of whether local development strategies have the desired effect. Additionally, Most Dynamic Metropolitans aids public-policy groups, elected officials, academics, businesses and other researchers monitor and assess metropolitan dynamism across the nation.

The Most Dynamic Metropolitan rankings are generated using performance-based metrics such as job growth, average annual earnings and Gross Domestic Product (GDP) gains, as well as new metrics: the proportion of total jobs at young firms and the educational attainment of employees at young firms. The young firm employment ratio influences economic growth as new firms develop new products, services, and advanced innovation. It encapsulates information on entrepreneurs’ capability to start businesses and scale them—critical for future job and

wage gains.

For example, just two metros out of the top 30 and 16 out of the top 100 have a young firm share below the mean of all metropolitan areas.

Educational attainment, particularly securing a bachelor’s degree or higher, has been shown to increase innovation and idea generation within a region. Our inclusion of the share of employees at young firms with a bachelor’s degree or higher is, therefore, a way of estimating the innovativeness of the young firms; the hypothesis is that more highly educated employees make a firm more innovative, leading to more new products, services and/or efficiency gains within the firm. In other words, young firms with more highly educated employees should be more competitive and have a higher likelihood of survival.

We also include data on regional price parities from the Bureau of Economic Analysis (BEA). These regional price parities are indicating whether goods and services are generally more or less expensive than the national average. We use them to adjust income measures for varying inflation rates and differences in purchasing power across metropolitan areas. Per-capita personal income reflects these adjustments and can be viewed as a measure of longer-term economic development because it is the stock of all prior welfare improvements. In the context of COVID-19, our metrics include job momentum as evaluated between August, 2019 and August, 2020. This allows us to discern the economic fallout attributable to the pandemic.

KEY FINDINGS

Positioned first in Most Dynamic Metropolitans is Midland, Texas.

Located in the American Heartland, Midland held several top positions and had four other metrics among the top 10.

Midland is the Permian Basin capital that produces two in five barrels of oil in the U.S. The explosion in shale oil exploration activity drives the economy and the Tall City is the most reliant on oil activity in the nation. How long oil prices remain below $50 per barrel will impact its future ranking.

San Jose-Sunnyvale-Santa Clara, California, (Silicon Valley) is second overall. Its unparalleled technology innovation ecosystem placed it tops among metros with a population above 1 million. Its biggest challenge in the future will be high housing costs, thereby making it difficult to retain talent. The median housing price is $1.25 million and rents are astronomical. COVID-19 may accelerate remote work of its tech employees.

Provo-Orem, Utah, ranked third and has become an entrepreneurship haven. Over the last two decades, the region has experienced phenomenal technology sector growth building on STEM talent graduating from Brigham Young University located in Provo. The tech boom has attracted new residents to the region and supports an expansion of advanced manufacturing around technology components. The result has been one of the fastest GDP growth rates in the country.

Next, at fourth, is Boulder, Colorado, where the university’s presence combined with the entrepreneurial culture, an attractive setting, and easy access to outdoor recreation means that Boulder will remain an appealing location for skilled workers and firms seeking to employ their talent. In fifth, San Francisco-Oakland-Hayward, California, has experienced more rapid tech-fueled growth over the past five years than its neighbor down the peninsula, Silicon Valley. However, San Francisco will be among the most impacted by its tech firms permitting remote work.

Austin, Texas, is sixth and has acquired well-deserved international recognition as an economic development model worthy of study. Austin has the 11th highest concentration of high-tech industries in the nation. Seattle- Tacoma-Bellevue, Washington, seventh overall, continues unabated as it is among the most innovative places in the world.

Greeley, Colorado, is eighth and has a mix of food, fracking, wind turbines and several corporate facilities. The economy of Naples-Immokalee-Macro Island, Florida, (ninth overall) is resilient, has withstood natural disasters the last three years, and is fast growing. **St. George, Utah **(10th overall) is home to Zion National Park, world-class outdoor recreation options, and arguably the preeminent mountain biking event worldwide, Red Bull Rampage.

The villages, Florida, is 11th, followed by Bend-Redmond, Oregon, (12th), and have been two of the nation’s hottest economies over the past decade. Next are Madera, California, (13th), **Mount Vernon-Anacortes, Washington, **(14th), and Nashville-Davidson-Murfreesboro-Franklin, Tennessee (15th). Boise City, Idaho (16th), which was second among medium metros (population of 500,000 to 999,999), followed by Idaho Falls, Idaho. Salt Lake City, Utah (18th), Denver-Aurora-Lakewood, Colorado (19th), and Fort Collins, Colorado (20th), round out the top 20. Fayetteville-Springdale- Rogers, Arkansas-Missouri was third among medium metros.

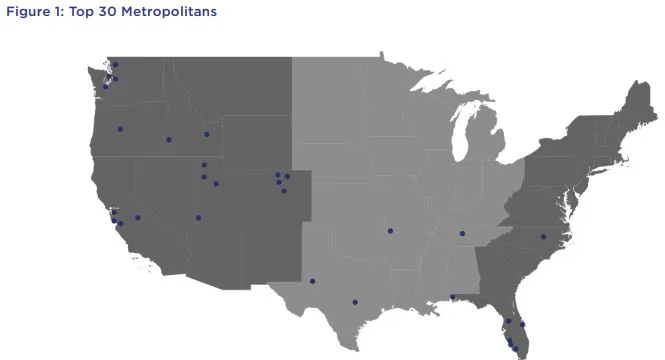

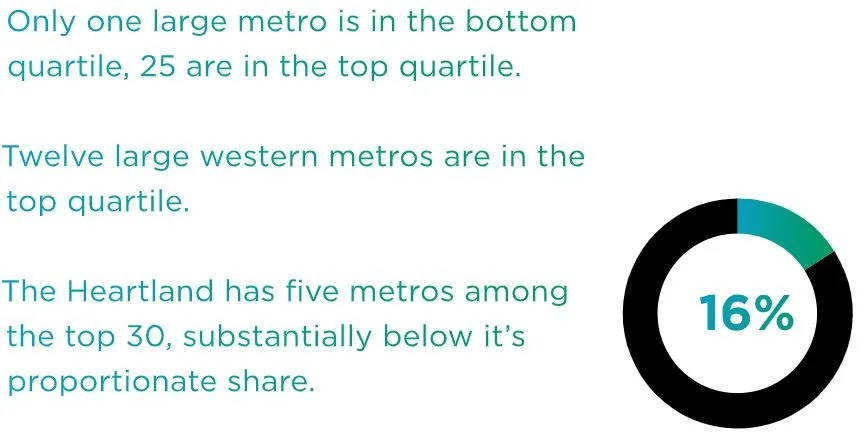

Other striking features of the findings include that only one large metro is in the bottom quartile; 25 are in the top quartile. Twelve large western metros are in the top quartile. The Heartland has five metros among the top 30, substantially below its proportionate share.

INDUSTRY CHARACTERISTICS

Common industry and structural characteristics separate top-performing metropolitan areas from lower performers over the evaluation period. Metropolitan areas with thriving professional, scientific and technical services were among the leaders.

Categories such as scientific research services, engineering services, accounting and business management consulting services are in this mix. These sectors have been among the fastest-growing industries since 2012. Another group of industries boosting growth in many metropolitan areas are information and communication services, data processing services and hosting services, cloud-based software, data visualization software, computer systems design, AI and machine learning, mobile applications, web design, internet publishing, social media, digital media and gaming software.

Other key industries differentiating the top from the bottom performers are research and development sectors, especially those involving physical and life sciences. The need for disease cures, effective treatment options and monitoring ongoing chronic conditions are powering research into drugs, diagnostics and a range of medical devices. High-tech and advanced manufacturing output has rallied since the Great Recession thrusting many metropolitan economies forward. High-tech manufacturing includes semiconductors, electronic instruments, computers, communications hardware such as routers and switches, energy-related cleantech, aerospace and aircraft, automotive, battery manufacturing, industrial control systems and material sciences.

Travel and tourism, recreation and lifestyle activities have advanced at a strong pace in recent years. Consumers postponed travel and tourism purchases during the Great Recession of 2007-2009. Pent-up demand for travel and tourism was unleashed when the economy improved. Domestic tourism destinations featuring outdoor adventures, such as those located near National Parks, benefited most, even during the pandemic; event-and attraction-based tourism, as well as air travel and cruises, have faced onerous restrictions in light of COVID-19, leading to reduced hours, layoffs and venue closures. Agriculture and food and beverage manufacturing also contributed to increased tourism, as producers identified niche and novel products and experiences to share with tourists, such as craft breweries and distilleries.

Metropolitan areas dependent upon coal mining have faced economic difficulties. With a combination of cheap natural gas and renewables gaining share in the electricity generation industry, coal’s share of the energy portfolio has plummeted. Metropolitan areas with adjacent communities dependent on agricultural crop production have witnessed slower economic growth. Prices of agricultural products dropped since 2014, harming agricultural-based communities’ economic fortunes— most of whom reside in the American Heartland. The U.S.-China trade war has exacerbated these trends.

The continuance of the U.S.-China trade war was not the only interruption to supply chains this year. China’s response to COVID-19, shutting down factories in February and March, led to supply chain disruptions across most manufacturing industries as well. Such disruptions are causing some companies to reconsider production location decisions, and the U.S. Heartland, uniquely positioned with access to raw materials and distribution networks, may see the reshoring of some manufacturing employment over the next year or two.

STRUCTURAL CHARACTERISTICS

Structural characteristics of metropolitan areas differentiate top performers from the rest of the pack. Metropolitan areas with leading research universities and four-year colleges embedded within their business milieu recorded exemplary economic gains, holding other factors constant. Research universities are increasingly critical to metropolitan performance as their fundamental output—knowledge—is central to an economy driven by innovative endeavors.

A strong culture of entrepreneurship, buttressed by numerous public and private groups, boosted the overall metropolitan leaders’ performance. Metropolitan areas that support the expansion of entrepreneurs and small businesses are more dynamic and resilient in the face of structural change. Incubators, accelerators, and various spaces that provide services to new or recently established firms are essential. Supporting this conclusion is that just two metros among the top 30 and 16 out of the top 100 have a young firm share below the average of all metropolitan areas.

Providing early-stage finance such as crowdfunding, angel investment and venture capital fuels startup activity and scale-up. Angel investors and venture capitalists provide not mere money but smart money. They bring expertise in management, product development and marketing. Moreover, they offer partnering opportunities. Metropolitan areas with a portfolio approach to economic development perform better over the long term.

Metropolitan areas with multiple community colleges developing curriculum geared to local employers’ requirements gain a competitive advantage. Smaller metropolitan areas located closest to large metropolitan areas exhibit more vital economic growth and share in that prosperity. Stronger economic linkages create a spillover effect. The arts, cultural, recreational and lifestyle amenities provide substantial advantages for metropolitan areas. They retain more residents who might otherwise seek career opportunities in other locations.

HEARTLAND IMPLICATIONS

While the Heartland has several metropolitan areas among the top performers, most metropolitan areas need to participate more fully in the knowledge-based economy. Technology sectors are underrepresented, too many economic development resources are devoted to smokestack chasing—heavy manufacturing recruitment, and too little emphasis is placed on supporting entrepreneurs. Financiers must become comfortable investing in early-stage firms in non-traditional sectors and more research universities need to embrace and pursue commercialization as a key component of their mission. The educational attainment and skills of residents must advance. A compelling narrative over the advantages of Heartland locations—such as lower housing costs and population density, access to raw materials, and distributional efficiencies—needs to be developed and conveyed for retaining and recruiting talent, especially in light of the COVID-19 pandemic.

INTRODUCTION

Metropolitan Statistical Areas capture the preponderance of economic activity in the United States. If metropolitan areas are not performing well, growth in the American economy will stagnate.

Further, innovative activities such as research and development and patenting are concentrated in metropolitan areas. The U.S.’s long-term potential output is underpinned by the mechanisms determining economic growth at the metropolitan level. Consequently, it is critical to discern those factors and share best practices of top-performing metropolitan areas so that other regions can evaluate whether emulating some best practices could boost their economic performance.

The Most Dynamic Metropolitan Index is an objective measure of the economic vibrancy of metropolitan areas across the nation. The Most Dynamic Metropolitan Index seeks to provide fact-based metrics on near-term and medium-term performance and prospects for long-term growth. There is a variety of potential applications for this index. The index allows economic development officials to monitor their metro’s vitality relative to others on a national basis or within their region and state. While international and national economic and geopolitical factors can influence growth patterns, the index provides an objective measure of whether local development strategies have the desired effect. Additionally, Most Dynamic Metropolitans aids public-policy groups, elected officials, academics and other researchers and businesses to monitor and assess metropolitan dynamism across the nation. If economic outcomes are not benchmarked, it is difficult to understand how a region is performing. Most Dynamic Metropolitans provide that benchmark, allowing change-agents to discern and address economic weaknesses.

Metropolitan areas can pursue various economic development strategies to achieve their goals for business expansion, job creation, income generation and expanding their tax base. Each metropolitan area must establish its pathway forward but should be aware of what factors have contributed to the success of other communities. We believe that the Most Dynamic Metropolitans provides additional information to help metropolitan areas improve their economic performance. The written analysis in this document is very detailed and provides a thorough perspective on what is working.

We utilize the metropolitan statistical area definitions developed by the U.S. Office of Management and Budget (OMB), based upon OMB Bulletin 18-03 (released April 10, 2018) for consistency with data sources. A metropolitan statistical area (MSA) is defined as a region having a large population nucleus, containing at least 50,000 people, with an adjacent population bearing a strong degree of economic and social interaction, including such measures as commuting patterns. Metropolitan areas are groups of counties. Data availability allows us to include 375 MSAs in our analysis.

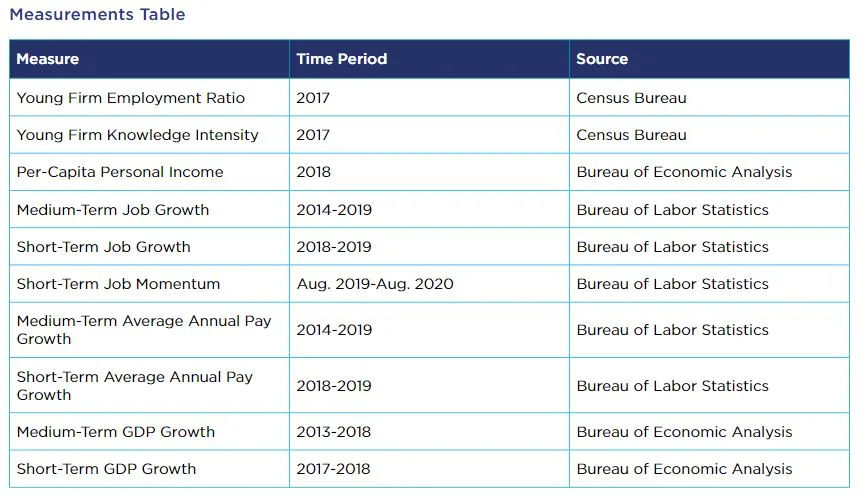

The Most Dynamic Metropolitan rankings are generated using performance-based metrics such as job growth, wage and Gross Domestic Product (GDP) gains, proportion of total jobs at young firms and the share of employees at young firms with a bachelor’s degree or higher.

The set of criteria is consistent with that used in our Most Dynamic Micropolitan Index.(super: 1) The last two measures capture which metropolitan areas are building economic opportunity for their residents and those who might desire to migrate. Our index is comprised of three types of metrics: recent economic development metrics and backward-and forward-looking metrics of longer-term economic development.

Recent economic development measures are 2018-2019 average annual pay growth, 2017-2018 real GDP growth, 2018-2019 job growth and job growth over the most recent 12 months ending in August 2020. Measures of longer-term economic development are the 2018 level of per-capita personal income, 2014-2019 growth in average annual pay, 2013-2018 growth in real GDP, 2014-2019 job growth, the 2017 ratio of employment at firms five years or younger to employment at all firms (young firm employment ratio), and the 2017 share of young firm employment with a bachelor’s degree or higher level of education (young firm knowledge intensity). The level of per-capita personal income can be viewed as a measure of longer-term economic development because it is the stock of all prior welfare improvements.

The young firm employment ratio has implications for future economic growth as new firms develop new products and drive innovation. It provides information on entrepreneurs’ ability to start new businesses and scale them—critical for future job and wage gains. Higher educational attainment can indicate a higher potential for new ideas and innovations. Young firm knowledge intensity, then, suggests the potential for young firms to innovate and bring new products and services into the marketplace. Each metric’s time period is restricted to data availability, with the most recent data incorporated and longer-term growth rates having a five-year span.

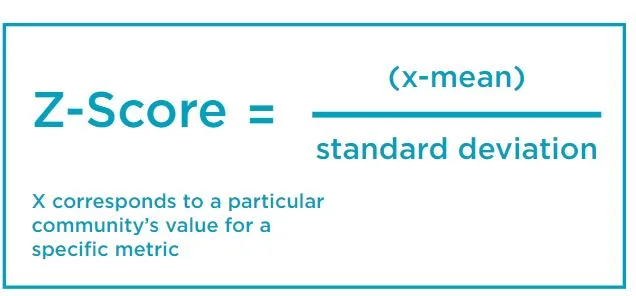

We standardize all metrics via z-scores. That is, we calculate the mean and standard deviation of a metric across all metropolitan areas, subtract the mean of the metric from each metropolitan area’s metric value, and divide that difference by the standard deviation of the metric. The result is a number telling us how many standard deviations above the mean (positive z-score) or below the mean (negative z-score) a metropolitan area’s metric value is. A metropolitan area’s index value is its average z-score across all ten economic development metrics. If a metropolitan area has a positive average z-score, then, on average, it performs better than the mean metropolitan area for each metric.

While most of our metrics are commonly used indicators of economic development, the young firm employment ratio and young firm knowledge intensity are relatively new measures. As presented in “Young Firms and Regional Economic Growth,”(super: 2) our analysis demonstrated that increasing the young firm employment ratio of the average metropolitan in 2010 by one percentage point led to an increase in private employment growth of half of one percentage point between 2010 and 2017; similarly, increasing young firm knowledge intensity of the same metropolitan area by one percentage point in 2010 led to an increase in private employment growth of nearly one percentage point between 2010 and 2017. These results clearly illustrate that a substantive relationship exists between young firms, higher education, and long-term private employment growth.

Additionally, we incorporate recent data on regional price parities from the Bureau of Economic Analysis (BEA) in our per-capita personal income and average annual pay metrics. These regional price parities are indexes indicating whether goods and services are generally more or less expensive than the national average. Therefore, the indexes can be used to adjust income measures for differing inflation rates and differing levels of purchasing power across regions.

OVERVIEW

Many of the top-performing metropolitan areas share common industry and structural characteristics, separating them from lower performers over the evaluation period. Perhaps the most important differentiator was the degree to which metropolitan areas participated in knowledge-intensive, high value-added industries that hire an above-average share of employees with advanced degrees and heavily invest in research and development. This manifests itself in high-tech service categories such as telecommunications and information services and specific manufacturing. Tourism was also a significant industry in the top-performing regions, reflective of their proximity to natural amenities. Growth in these industries also caused growth in transportation services and construction in these regions. West Coast metros benefitted the most from this industry composition, but some East Coast and Heartland locations are among the mix.

INDUSTRY CHARACTERISTICS

Metropolitan areas with flourishing professional, scientific and technical services were boosted in the rankings. These include categories such as scientific research services, engineering services, accounting and business management consulting services. Professional, scientific and technical services have been among the fastest-growing industries since 2012. Metros with a high concentration of these activities were bolstered by the secular shift underway in the national economy. Examples of communities include San Jose, Austin, San Francisco, Seattle, Raleigh, Boulder and Denver. Professional and technical services serve as important anchors for communities with a high concentration as they pay above-average wages and provide strong economic spillovers. Professional, scientific and technical services shape growth across a broad swath of communities.

Information and communication services, data processing services and hosting services, cloud-based software, data visualization software, computer systems design, Artificial Intelligence (AI) and machine learning, mobile applications, web design, internet publishing, social media, digital media and gaming software are another group of industries propelling growth in many metropolitan areas. These sectors are creating high-paying jobs at a prolific rate in the United States as the demand for these activities proliferates. These industries have a high multiplier effect on local economies. In many cases, three to four other jobs are generated by one job in these sectors. Metros with a strong concentration, and the ability to expand them, are reaping the rewards. At the top of this list is San Francisco, closely followed by San Jose, Provo, Denver, Seattle, Austin, Boulder, Nashville, Raleigh and Salt Lake City.

Other key industries differentiating the top from the bottom performers are research and development sectors, especially around life sciences. The demand for cures to disease, effective treatment options and monitoring ongoing chronic conditions are driving research into drugs, diagnostics and a range of medical devices. This research requires extensive scientific, medical and technical expertise. Most of these occupations pay in excess of $150,000 annually. Several of the top 30 metros have university research centers with expertise in the life sciences, especially in biotechnology. For example, in the Idaho Falls metro area, life science and engineering research and development are almost 17 times greater than the U.S overall. Boulder, Raleigh, Salt Lake City, San Francisco and San Jose also have large concentrations of these biomedical activities.

A rebound in high-tech and advanced manufacturing since the Great Recession has thrust many metropolitan economies forward. Semiconductors, electronic instruments, computers, communications hardware such as routers and switches, energy-related cleantech, aerospace and aircraft, automotive, battery manufacturing, industrial control systems and material sciences are among high-tech manufacturing. The high-wage occupations associated with these industries have strong ripple effects across the regional economy. Furthermore, they provide middle-class jobs for many technical professions that do not require a four-year college degree. Boise City, Boulder, Austin, Greeley, Seattle, Provo, Palm Bay and San Jose are among those metros supported by the expansion in these manufacturing sectors.

Travel and tourism, recreation and lifestyle activities have advanced at a strong pace in recent years. Travel and tourism purchases were delayed during the Great Recession of 2007-2009. Pent-up demand for travel and tourism was generated and when the economy improved, these deferred purchases accelerated. This was especially the case for tourism-destination locations where visitors travel long distances to enjoy their amenities. The resurgence in these sectors was aided by the preference for experiential experiences of millennials. The Millennial age cohort allocates less of its consumption toward hard assets and more toward soft amenities.

At the top of the list of places benefitting from travel and tourism, recreation and lifestyle activities—at least before the pandemic—are Heartland-located Nashville, Tennessee and Fayetteville, Arkansas-Missouri. Nashville is home to the Ryman Auditorium—home of the Grand Ole Opry—and other legendary country music venues. At the same time, Fayetteville-Springdale-Rogers, Arkansas-Missouri has become a mountain bikers haven, among other outdoor activities. Other smaller metropolitan areas such as Bend, Oregon; Saint George, Utah; Fort Collins, Colorado; Boise City, Idaho, and Daphne, Alabama are in this group. Larger metropolitan areas such as Naples, Florida; Cape Coral-Fort Myers, Florida; and Seattle were also experiencing gains.

Contributing to the tourist amenities in some locations is agriculture and food and beverage manufacturing. Metropolitan areas with adjacent communities dependent on agricultural crop and animal production, as well as food and beverage manufacturing, performed well in this year’s rankings. Despite low prices for agricultural products and harmed the economic fortunes resulting from the U.S.-China trade dispute, niche and novel products as well as growth in the local and regional food movements —including craft breweries and distilleries—contributed to employment and GDP growth in nearly half of the top 30 metropolitan areas. Madera, California, Santa Cruz-Watsonville, California, and Mount Vernon-Anacortes, Washington led with exceptionally high concentrations of employment in agriculture, while Bend, Oregon has a high concentration of employment in forestry and logging and beverage manufacturing. Greeley, Colorado, Fayetteville-Springdale-Rogers, Arkansas, and Fort Collins, Colorado also have strong food and beverage manufacturing sectors from which they benefited.

Oil prices recovered from 2012 to 2015 but collapsed again in 2016, harming metropolitan areas’ economic performance with a heavy reliance on exploration and the downstream pipeline. The exception being metropolitan areas with high productivity shale deposits or those located close to them. Overall first-place, Midland, Texas, is the capital of the Permian Basin, the most productive basin in the U.S. Greeley, Colorado, and Mount Vernon-Anacortes, Washington, also benefited from the oil boom. However, they are experiencing contractions in the energy sector due to persistently low oil prices associated with reduced fuel demand during the COVID-19 pandemic.

A critical restraint on economic advances across a swath of metropolitans was a high dependence on mining activity, principally coal mining. Coal’s share of electricity generation has plummeted in recent years as natural gas has replaced it in the generation mix and renewables have gained market share. This has affected metropolitan areas in the eastern and western interior. Charleston, West Virginia, Cumberland, Maryland, and Beckley, West Virginia, all three falling in the bottom quartile of the rankings, are examples of metropolitan areas feeling the ill effects of declining coal production. Additionally, communities reliant on commodity agriculture have struggled in the face of unseasonal flooding and the U.S.-China trade war that has limited agricultural exports to China.

STRUCTURAL CHARACTERISTICS

Key characteristics separating top-performing metropolitan areas from their colleagues are structural. Metropolitan areas with leading research universities and four-year colleges embedded within the regional business milieu recorded exemplary economic gains, even after adjusting for other determinants. Research universities become ever more critical to metropolitan performance as their fundamental output—knowledge—is central to an economy driven by innovative endeavors.(super: 3) The best create substantial talent, particularly in STEM fields; license their IP to established firms or startups, and business engagement by consulting and sharing tacit information. One measure of universities and colleges’ importance to economic growth is the share of employees with a bachelor’s degree or higher at firms 5 or less years old, or what is referred to as young firm knowledge intensity elsewhere in this report.

Several metropolitan areas with research universities—critical components of their metropolitan area’s innovation ecosystem—were among the Most Dynamic Metropolitans’ leaders. These include Stanford, a uniquely entrepreneurial institution assisting in driving the San Jose metropolitan area; the University of Texas-Austin in the Austin metro area; the University of California, Berkeley and the University of California, San Francisco in the San Francisco metro area; the University of Washington in Seattle; Brigham Young University in Provo-Orem; Vanderbilt University in Nashville; the University of Colorado-Boulder; Colorado State University in Fort Collins; the University of Arkansas-Fayetteville in Northwest Arkansas; North Carolina State University in Raleigh and University of California at Santa Cruz. Among others, these universities had faculty engaged in the commercialization of their research and founded companies that led to job creation. Much of their impact was in technology-based industries—additionally, human capital assists in attracting knowledge-intensive firms.

Metropolitan areas with a culture of entrepreneurship supported by numerous public and private groups are among the overall leaders and improved several others’ performance. A measure of entrepreneurship and scale-up success, the share of total employment represented by firms five years of age or fewer, is included in our metrics for Most Dynamic Metropolitans. While it should not be a surprise that metros scoring high on this measure performed well in our index since it is among the metrics, the relationships are intertwined and seemingly causal in nature. By examining other measures of economic performance such as job growth and gains in real GDP, they are closely correlated with metros with a high percentage of total employment at young firms. Only two metros out of the top 30 and 16 out of the top 100 have a young-firm share below the mean of all metropolitan areas. Metropolitan areas that support entrepreneurs and small businesses in expanding are more dynamic and resilient in the face of structural change. Incubators, accelerators, and various spaces that provide services to new or recently established firms are essential.

Access to early-stage financings such as crowdfunding, angel investors and venture capital fuel startup activity and scale-up. Angel investors, and venture capitalists in particular, provide not mere money but smart money. In other words, they have expertise in management, product development and marketing. Moreover, they offer partnering opportunities. San Francisco and San Jose have access to the densest venture capital located on Sand Hill Road. However, rising venture capital availability in Austin, Denver, Provo, Seattle and Raleigh is spurring growth. Local angel investors are assisting smaller areas such as Bend, Oregon, and various other Most Dynamic Metropolitans.

Metropolitan areas with a portfolio approach to economic development seem to perform better, in a fashion similar to that found for micropolitan areas. From our Most Dynamic Micropolitans, “Communities actively recruiting firms from other locations to relocate or start local establishments appear to achieve stronger economic growth. Also, their approach supports indigenous expansion and startup activity. Communities with economic development officials actively engaged in scanning for best practices in regulatory and tax policies, technical assistance, strategies for workforce development and business retention and recruitment exhibit stronger economic growth.”(super: 4)

Metropolitan areas with multiple community colleges developing curriculum geared to local employers’ requirements seem to gain a competitive advantage. Employers must adjust to alternations in skill requirements within their industries to be competitive. Community colleges that quickly adapt curriculum lend support to their students in obtaining local employment. Apprenticeship programs established at local firms linked to the curriculum at community colleges and certification programs assist retention of graduates.

Smaller metropolitan areas located closest to large metropolitan areas that are exhibiting stronger economic growth share in that prosperity. Stronger economic linkages create a spillover effect. Access to sophisticated business services, adjacent angel and venture capital availability, supply-chain relationships and numerous other interactions explain the advantages of proximity. On average over the period of the study, large metropolitan areas (population of one million or above) recorded higher economic advances than smaller ones.

The arts, cultural, recreational and lifestyle amenities provide substantial advantages for metropolitan areas; particularly, research points toward smaller communities that emphasize them early during the growth cycle reach a 750,000-population threshold sooner. They retain more residents who might otherwise seek career opportunities in other locations. Quality of place also includes good K-12 education, access to quality health care, low crime rates, and various other factors. A growing body of evidence suggests a correlation between arts and culture and economic success.

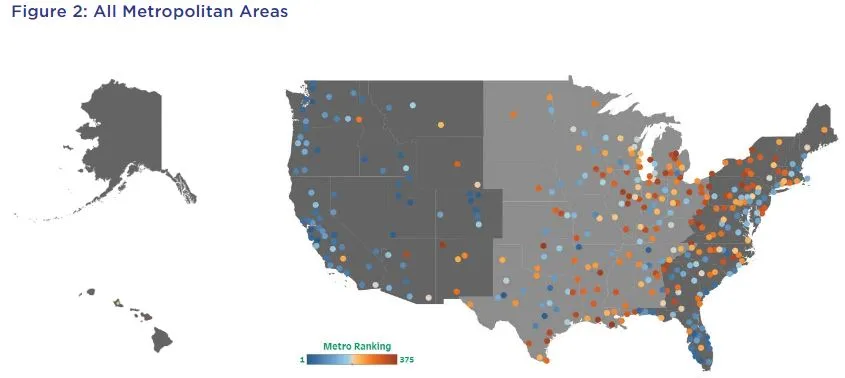

ALL METRO RANKINGS

Displays a map of all 375 metropolitans areas included in our analysis. The map color-codes the metropolitan areas from dark blue (highest rank) to burgundy (lowest rank); white represents the median metropolitan area—ranked 188th. The pattern of colored dots is explained by the combination of the industry and structural characteristics highlighted above. Only five metropolitan areas are in the Heartland are in the top 30 and featured herein; an additional 11 metropolitan areas located in the Heartland are found in the top 100. If they represented their share among all metros in the nation, there should be 39.

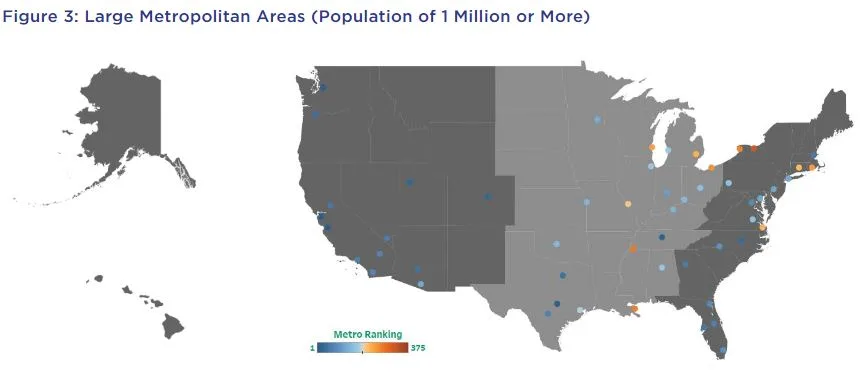

LARGE METRO RANKINGS

Displays the large metropolitan areas (population one million or above) represented by their distribution among all metros. Most striking is that only one large metro is in the bottom quartile of performers, while 25 are in the top quartile (their proportionate number would be just eight). The Heartland has four large metros in the top quartile. Only one of the 13 large Western metros is not in the top quartile.

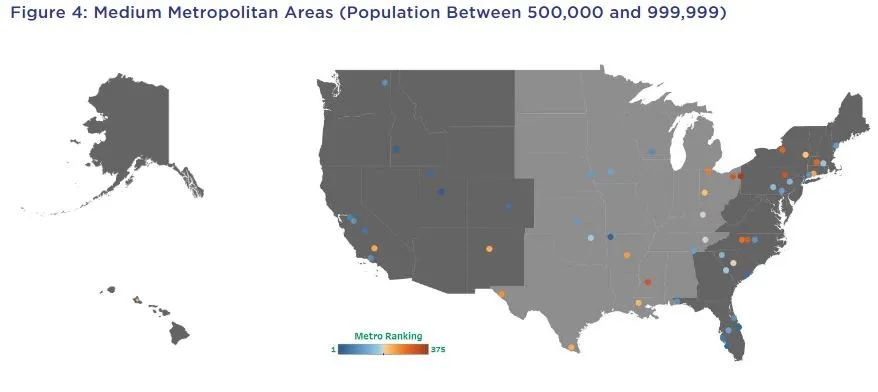

MEDIUM METROS

Displays the medium metropolitan areas (population 500,000 to 999,999) represented by their distribution among all metros. The Heartland has two out of 19 medium metros in the top quartile, while the Western metros have 9 out of 12 medium metros in it.

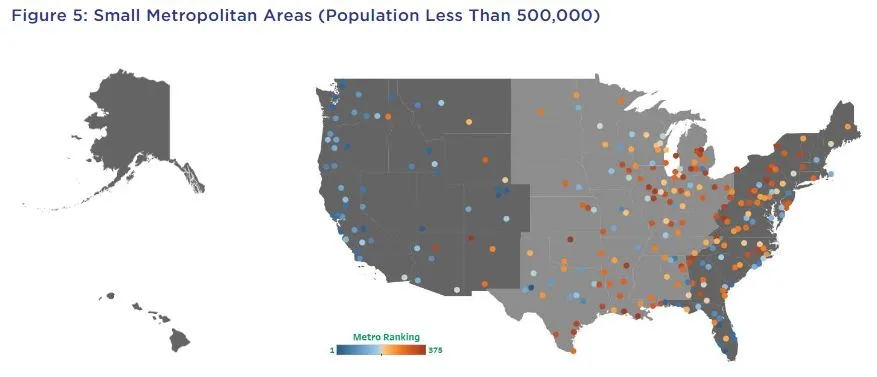

SMALL METROS

Despite a substantially lower number of small metros in the West than in the Heartland, the West had 27 among in the top quartile, while the Heartland had just eight.

Midland, Texas, retained the top position in Most Dynamic Metropolitans.

The rapid expansion in shale oil over the past five years has propelled Midland’s economy. As the capital of the Permian Basin—the most productive structure in the nation—it has reaped the benefits of rapidly expanding exploration in its own geography; and as the provider of technology and oil service support firms to communities throughout the region. The high proportion of overall economic activity attributable to oil exploration and support functions drives the regional economy. For example, real GDP in Midland rose 23.5 percent in 2018—the highest in the nation. Real GDP growth in the five years through 2018 exceeded all metropolitan areas in the nation.

The global economic fallout from COVID-19, and the associated drop in oil demand, precipitated a collapse in oil prices. Declining Permian exploration and $40 barrel prices create an abrupt contraction in Midlands economic activity. Nevertheless, the long-term prospects for the region remain favorable.(super: 5) The breakeven oil price in the Permian has fallen to around $47 per barrel, with some analysts claiming it may be as low as $33—the lowest in the nation.(super: 6)

Across all of the nine metrics in our evaluation, Midland’s performance was more than three standard deviation units above the metropolitan average, this includes the decline in jobs between August 2019 and August 2020. Being more than three standard deviations above the average metro is an extremely rare occurrence as compared to the second-ranked metro which is two standard deviations above the mean. Midland was first in four metric categories and in the top ten in two other categories.

The Permian Basin produces one in five barrels of oil in the U.S.(super: 7) There is no community whose fortunes are more closely tied to oil exploration and production activity than the Tall City.(super: 8) Oil and gas extraction and support activities for mining are 73 and 57 times, respectively, more important to Midland than for the U.S. overall. Just a decade ago, the Permian Basin was in remission and Midland’s economic prospects diminished. The synchronized development of horizontal drilling technology and advances in hydraulic fracturing techniques, merged with some of the thickest shale deposits in the U.S., have changed Midland’s wealth and the communities of the Permian Basin.

Many believe that production will eclipse the Ghawar field in Saudi Arabia, the world’s largest, within three years. Even today, Permian oil production exceeds all 14 members of OPEC other than Saudi Arabia and Iraq.(super: 9) Some Midland officials have warned that the boom-and-bust cycles of the past could return. Drilling activity is dependent upon the price of oil. COVID-19 contraction has been severe, but the ripple effects across the economy have been less onerous than in the past. However, the ultimate economic fallout rate will be determined by how long oil prices remain below $50 per barrel.

The multiplier effect of oil exploration and production on the supply chain induces a positive influence on ancillary services. Average annual earnings in oil exploration in Midland was $96,000 in 2018—double the non-energy wage. High wages are paid to professionals at petroleum engineering service firms like BCCK Engineering, Dawson Geophysical Company and Hy-Bon Engineering because they possess specialized knowledge on the latest technological advances in geologic sciences used in the fracking industry. Specialized software firms, such as Enertia Software, support oil exploration and are part of the activity’s dense cluster.(super: 10)

Oil, ranching, agriculture, healthcare and transportation remain economic pillars; however, focused efforts on diversifying its economy are underway in Midland. Strengthening its entrepreneurial ecosystem is a key focus. Midland improved its positioning to second on the young firm share of total private sector employment. This is up six spots from the previous year. It would behoove Midland to devote time to boost the knowledge intensity of startups in the area.

Role models that can serve as mentors are critical and Midland has a compelling female entrepreneurial-success story to tell. Susie Hitchcock Hall, the founder and owner of Susie’s South Forty Confections, makes custom candies, and is well known for its Texas Pecan Toffee that ships around the world.(super: 11) The Roden Entrepreneurial Development Center at the University of Texas, Permian Basin (UTPB) promotes building entrepreneurial skills. The program helps students develop a standard frame of reference to commercialize innovative ideas best described as “Real Business” projects.(super: 12) UTPB has a business plan competition called the Entrepreneurial Challenge. After qualification, entrants have access to pertinent resources like one-on-one business coaching. Midland also supports black businesses with the African American Chamber of Entrepreneurs, Inc.

An emergent economic engine in Midland is in Aerospace. The Spaceport Business Park, located at the renamed Midland International Air & Space Port, claims to be the first located at a major commercial airport. The facility is FAA-approved, which is attractive to satellite firms, whether in the testing, producing, or launching segments. It has attracted a technology firm and another that manufactures and launches satellites.(super: 13) The Midland Altitude Chamber Complex supports the testing and qualification of space and pressure suits, payloads, components and trains new flight crews. RBC | Sargent Aerospace & Defense, a leading provider of precision-engineered customized components and aftermarket aviation services, has expanded in the metro area and several other aerospace suppliers are establishing operations.

Employment in Midland in August 2020 was 13.7 percent lower than in August 2019 reflecting the impact of reduced energy activity. Mining, logging and construction jobs were down 28 percent over the same period. However, efforts are underway to mitigate the effects. Consolidation in the industry is taking place to restructure and survive the coronavirus pandemic. Pioneer Natural Resources, the area’s largest employer, purchased Parsley Energy Inc . in an all-stock deal.(super: 14) A number of transactions are taking place, which should improve firms’ capital structure and cut operating costs. The Clean Economy Jobs and Innovation Act passed the House of Representatives. It aims to support research and development funding and finance clean energy initiatives such as the 1Pointfive carbon sequestration project proposed by Oxy Low Carbon Ventures and Rusheen Capital Management.(super: 15) The Midland Development Corporation developed a creative small business assistance program to help local businesses survive the pandemic. Businesses can apply for up to $25,000 in loans that can qualify for forgiveness.(super: 16)

The Midland Chamber of Commerce understands that quality of place is a business and talent attraction and retention tool. Midland has a vibrant art and cultural scene that attracts and retains skilled workers and their families. The Midland Performing Arts Center is regarded as one of the best for a community of its size and is home to the Midland Symphony Orchestra.

(image: midland-metric-table.jpg)

**San Jose-Sunnyvale-Santa Clara, California remained second overall and first among large metropolitan areas. **

Silicon Valley has seen its rate of job creation diminish over the past several years. Still, high wages associated with the high-tech workforce provides an enormous multiplier impact on the economy. Additionally, wealth creation is spurred by stock options’ generous use at its startups and mature tech firms. The San Jose metro area led the nation in gains in real average annual pay between 2014 and 2019. An estimated 29.6 percent of employment in the metro area are high-tech industries—nearly six times greater than the U.S. average.(super: 17) COVID-19 in 2020 is adversely impacting its economy with foreign travel restrictions that are devasting the service industry that is dependent on leisure visitors. Along with San Francisco, the San Jose metro has the strongest ties to Asia and, in particular, China. However, high-tech employment is down just 2.1 percent from February 2020.

The metro area is the global capital of innovation. The unique combination of leading research universities focused on commercialization, engineering acumen and pioneering in the life sciences, extensive risk capital, dense business networks aligned with a risk-taking and entrepreneurial culture to fuel an innovation-driven economy.(super: 18) Its IT hardware discoveries are legendary, but its recent innovation breakthroughs are in the softer side of technology including: AI, machine learning, cloud computing, data processing and hosting services, web design, social media, blockchain technology, autonomous vehicles and advances in medical science that are keeping the region on an expansion path over the long haul.(super: 19)

San Jose ranks among the top performers across several metrics. In addition to being first in medium-term average annual pay growth, it leads the nation in the knowledge intensity at young firms with 39.6 percent of employees with a bachelor’s degree or higher. San Jose is second on two metrics and in the top five on two others in our analysis. San Jose’s per capita income is fourth in the nation. An astonishing 26 percent of San Jose households earn more than $200,000 annually and 39 percent earn $150,000 or above.(super: 20)

The high-skilled workforce fuels, and is fueled by, the symbiotic relationship that exists with the broad employment category of professional, scientific and technical services, the largest category in the San Jose metro. Between 2014 and 2019, professional, scientific and technical services added 28,200 jobs. Other information services created 19,200 jobs from 2014 to 2019, the most of any metro in the nation, and the preponderance was in cloud computing. One rapidly growing startup in this space is Cohesity, Inc.; the firm quadrupled its global employees in 2018.(super: 21) Even traditional communications equipment makers are entering this market with Broadsoft, a communications software firm, acquired by Cisco for $1.9 billion in late 2017.(super: 22)

The travel bans and restrictions on reopening business attributable to COVID-19 had a devastating ripple effect throughout the region’s economy.(super: 23) More than 150,000 jobs were lost between March and April and less than half of those jobs have been recovered. Employment in August 2020 was 8.3 percent lower than in August 2019. The unemployment rate rose from an extremely low 2.5 percent in February to 12.0 percent in April. It declined to 7.4 percent in August. However, job postings remained high at 93,841 in September, according to Emsi. The number of passengers screened by TSA in the metropolitan area fell from 496,163 in February to just 126,395 in September, a 74.6 percent decline(super: 24)

San Jose’s unique innovation ecosystem and the ability to pivot to new growth sources will cause a rapid recovery. For example, venture capital investment in health is accelerating. Stanford is a bedrock of Silicon Valley’s high-quality university research and commercialization with a unique breed of entrepreneurial undergraduates, graduate students and faculty fueling its economy. San Jose State University has one of the top-ranked computer science programs in the country courtesy of major tech firms’ investments.

Tech stalwarts Alphabet, Apple, Cisco, Facebook, Hewlett-Packard, Intel and Oracle invest a high share of their revenues back into R&D in an attempt to keep ahead of the newly emerging competition that might disrupt their current lines of business. Further, they invest in early-stage firms (captive venture capitalists (VCs) that they may later acquire to develop a new product or service offering. Some might argue this practice stifles the growth of future competitors. The U.S. Department of Justice feels this is the case.

Many employees of large tech firms go on to establish their enterprises, underpinning an entrepreneurial culture. A disproportionate share of these tech entrepreneurs were foreign-born. Studies performed by Joint Venture Silicon Valley indicate that approximately 40 percent of tech firms had at least one foreign-born founder. Research and development (R&D), technology transfer, patenting, angel investing, venture capital, management talent, initial public offerings (IPOs), mergers and acquisitions (M&A) and market capitalization are the capstones of the regional innovation ecosystem.(super: 25)

Most Sand Hill road-based VCs do not want to fly to the center of the U.S. It is hard to argue with this perspective as the density of knowledge creation in Silicon Valley provides numerous opportunities for investing, and they can manage a broader portfolio of firms. Data from the Census Bureau for 2019 show that 53 percent of the region’s 25 or older residents have graduated from college. A remarkable 25 percent hold an advanced degree, contrasted to only 13 percent in the U.S. population overall. Venture capital funding became even more concentrated in Silicon Valley and the surrounding region in 2018. Silicon Valley and San Francisco venture capital investments dropped to $42 billion ($18 billion in Silicon Valley) in 2019, representing 40 percent of all venture placements in the nation.(super: 26) However, early-stage angel investing declined substantially in 2019, indicating that the next generation of tech firms may not evolve at the same pace.

The friction generated by the scale of economic activity in a dense peninsula is causing the centrifugal forces to limit future growth. Silicon Valley has not added new housing units at a pace fast enough to house the new jobs. Perhaps the current COVID-19 retrenchment will provide an opportunity to close this housing gap. Residents fear that more housing will lead to even-greater congestion problems. Because housing costs are beginning to outstrip compensation gains for many workers, Silicon Valley had a net domestic migration of negative 26,000 in 2019. What has become a challenge for Silicon Valley is now becoming an opportunity for non-coastal sections of the country with lower housing costs, especially given the ability to work remotely. Expect San Jose to see its ranking drop in future years.

(image: san-jose-metric-rank-able.jpg)

The Provo-Orem, Utah economy has gone from strength to strength over the past decade by leveraging local assets to create opportunity.

It outperformed every other mid-sized region on our index by a wide margin. It came very close to usurping the San Jose-Sunnyvale-Santa Clara region’s hold on the second-place berth this year. The region’s phenomenal technology sector growth has driven up both wages and GDP, and provided opportunities for the graduates from Brigham Young University (BYU). The STEM focus and the entrepreneurial culture at BYU and the broader Provo-Orem region help explain the large role young firms play in the local economy. Young firms provide more than 18 percent of jobs, the largest share among mid-sized regions on our index. This momentum carried the Provo-Orem region through the initial six-months of the COVID-19 pandemic; it is the only metro in the top five that managed to grow employment between August 2019 and August 2020.

The Provo metro is at the southern point of Utah’s “Silicon Slopes,” which has Salt Lake City at its center and then sweeps north through Ogden-Clearfield. Its key technology clusters are software publishers, semiconductor manufacturing, and computer systems design. These deeply rooted clusters continue to generate new opportunities for nascent firms through a vibrant startup culture and a willingness among successful founders to continue to invest locally. The list of locally grown success stories is long. Qualtrics International, a customer survey software provider, founded in Provo, was acquired by SAP for $8 billion.(super: 27) Domo was founded in 2010 by a BYU graduate and went public in 2018.(super: 28) Omniture, an online marketing and web analytics firm founded in Orem, is another example. It was acquired by Adobe in 2009, attracting the software multinational to the region. While venture capital is still concentrated on the east and west coasts, the homegrown Utah pool of capital fosters new waves of successful firms.

The region supports fledgling tech firms through its tech incubators like Startup DoJo, Boom Startup and Camp 4 group.(super: 29) Provo has several local angel and venture capital investors but attracts Silicon Valley venture capital investment as well. The National Federation of Independent Businesses ranked Provo second in the nation, after Austin, as a location to start a business.(super: 30) This dynamic startup environment helped Provo claim sixth place nationally for the proportion of total jobs at young firms, first among mid-sized metros.

These impressive tech industry gains have had significant spillover effects across the economy. Only five metropolitan areas had faster real GDP growth than Provo during 2019, creating an opportunity for the skilled regional workforce. No mid-sized metro added jobs faster than the Provo-Orem region over the past five years, and the competitive labor market has helped drive up average annual pay between 2014 and 2019, so that only the San Jose metro bested its pace over that period. These wage gains, in turn, have fueled overall consumption and housing gains.

Another result of this sizzling economy has been a steady stream of new residents moving into the Provo-Orem metro. The region’s population increased by more than 120,000 people between 2010 and 2019, with a quarter of that growth attributable to a combination of domestic and international in-migration.

Advanced manufacturing is also important to the regional economy. IM Flash Technologies, a subsidiary of Micros since late 2019, is located in Lehi and produces 20 percent of the world’s microchips. It is also a prominent player in nanotechnology.(super: 31) Firms like Boeing, Blend Tech, Klune Industries and Wavetronics also produce in the region.

Brigham Young University is central to the success of the metro area. BYU has expanded its student base and is creating more entrepreneurial STEM graduates. BYU was fourth in the nation among universities commercializing intellectual property through starting new firms or licensing the technology to existing ones.(super: 32) The presence of a young, educated population is a draw for firms looking to hire trained talent, and the family-focused work culture can help retain employees that seek work-life balance over maximum possible salaries. Utah County has the youngest median age in the country at 26.1 and millennials comprise 30 percent of its labor force while baby boomers represent just 12 percent.

Based in Orem, Utah Valley University (UVU) has a history as a vocational school. It maintains its ties to workforce training through its continuing education programs. Recently, UVU launched the Live and Work in UT program to help Utah residents who are either unemployed or underemployed and seeking short-term training for high-demand jobs. The program is funded by federal CARES act dollars in response to the COVID-19 pandemic and provided at no cost to students.

Like many regions with sizeable student populations, there are concerns about the pandemic’s impact on the census count and future federal funding.(super: 33 Students’ absence on campus also affects many firms that serve that population and depend on their spending. The region’s demographic profile suggests the pandemic may have less dire health consequences for the local and student population, allowing a swifter reopening than elsewhere in the country.

The rapid population and economic growth in and around the Provo metro have also fueled real estate development and construction. In addition to new housing, several major construction projects have been underway in recent years. In Orem, new retail continued to open in the University Place development.(super: 34) Adobe has been building Phase 2 of their Lehi campus, which broke ground in 2018. The four-story office building will provide an additional 160,000 square feet for the firm and incorporates 1,600 solar panels and other sustainable features. The building was due to open in 2020 and was being finalized when the pandemic hit.(super: 35)

As Provo continues to develop its high-tech hub and foster local entrepreneurship, it will begin to experience more of the challenges faced by established tech hubs. Strong housing demand has pushed up median home and rental prices, and the region is changing the zoning rules to address the issue.(super: 36) The area will need to maintain its house pricing, commute time and quality of life advantages, by focusing on a sustainable approach to development, broadening their transportation mode options and reducing congestion. Overall, the region is well positioned to emerge strongly from the pandemic.

(image: provo-table.jpg)

**Continuing its strong run, Boulder, in northern Colorado, ranks fourth by capitalizing on its stellar research and technology hub. **

Impressive local increases in average annual pay in the short- and medium-term ranked first among small metros, and its 2018 to 2019 performance on this measure beat every other metro on our index. Although the University of Colorado Boulder continues to deepen the pool of skilled graduates, the tightening labor market was beginning to slow the region’s growth. The university’s presence combined with the entrepreneurial culture, an attractive setting, and easy access to outdoor recreation means that Boulder will remain an appealing location for skilled workers and firms seeking to employ their talent.

The University of Colorado Boulder employs 7,000 faculty and staff and had a Fall 2019 enrollment of 34,500 students. With top tier programs in aerospace engineering sciences, physics, and geology, the university trains the technical workforce for the engineering and research laboratories in the Boulder region and beyond. The institution attracts significant research funding to the region, $614 million in the fiscal year 2020, from national funders like the National Science Foundation and the National Institutes of Health.(super: 37)

The students also contribute to the local economy through their consumption. However, their absence in the Spring semester of 2020 during the implemented stay at home restriction in response to the COVID-19 pandemic took a toll on local retail, leisure and hospitality spending. The pandemic’s broader economic impact is likely to affect the university’s public funding as the State budget is adjusted to reflect the new demands on limited public funds. Hopefully, these effects are temporary, as the need for scientists and engineers educated by the school will remain high.

Boulder’s performance in the index is built upon its innovation culture. Local institutions and researchers produced the fourth-most technology patents per capita from 2000 to 2015.(super: 38) In addition to the academics at the University of Colorado Boulder, the region is also home to multiple national research labs and other notable not-for-profit, tech-centric facilities. Among these are the National Ecological Observatory Network, the National Center for Atmospheric Research and related University Corporation for Atmospheric Research, the National Oceanic and Atmospheric Administration’s Earth System Research Laboratory, and the National Institute of Standards and Technology Laboratories.

The technology sector in Boulder is vast, encompassing high profile high-tech firms like IBM, which has had a presence in Boulder for decades and is one of the metro’s largest employers.(super: 39) Google has offices in Boulder. In 2019 the search giant partnered with the City of Boulder to develop an eligibility calculator for residents interested in identifying public programs for which they might qualify.(super: 40) It also includes high-tech manufacturers such as Medtronic, a global leader in medical device development and manufacturing that employs more than 1,500 people in the metro.(super: 41) Boulder is home to Ball Aerospace, a subsidiary of the jar-maker Ball Corporation that undertakes advanced manufacturing projects in fields ranging from national security to space exploration; the aerospace firm began a major fixed capital expansion in 2017.(super: 42) Like much of Boulder’s aerospace industry, the firm continued to add headcount even as the economy was affected by the COVID-19 pandemic. Blue Canyon Technologies, another aerospace firm in the Boulder region added jobs in 2020 after opening their new facility in Lafayette. (super: 43)

These high-tech sectors have attracted and retained a large pool of highly skilled workers, whose rising incomes contributed to the Boulder metro’s high ranking on our index. The per capita personal income in the region placed 11th in the nation, driven in part by the tightening labor market. The labor force’s share, providing professional, scientific and technical services was 19 percent in 2019, much higher than typical for the United States. Many of these employees were able to switch to remote work when required in response to the pandemic. More businesses in Boulder continued operating and the impact of job losses was smaller than in regions more dependent on industries based on in-person interaction or discretionary consumer spending as a result.

Boulder is also an entrepreneurial hub, building on the innovations generated at its research institutions. It ranks sixth for its new firms’ knowledge intensity, and young firms employ approximately 15 percent of the workforce. The research has yielded several vibrant startups that contribute to the metro’s high-tech economy. Email management platform creator SendGrid, founded and incubated in Boulder, went public in 2017 and was acquired by Twillo in 2019 for $3 billion.(super: 44)

A 2019 study estimated that through its technology transfer successes, the University of Boulder had an economic impact of $1.2 billion on the Colorado economy between 2014 and 2018.(super: 45)

Like the rest of Colorado, the Boulder economy benefits from its natural beauty and varied recreational opportunities. Boulder County is home to Longs Peak, one of the tallest mountains in the country. Boulder’s easy access to world-class outdoor amenities, including mountain biking, road biking, hiking, climbing, kayaking and skiing offers a high quality of life to those who want to get out into nature.(super: 46)The Boulder region was identified as the best place to live by U.S. News & World Report in 2020, with its high quality of life a major factor in its rating.(super: 47)

Over the past few decades, Boulder’s success and its expanding workforce have brought with them a tight housing market and skyrocketing housing costs. As in other successful tech hubs where new builds are limited, these housing costs create real hardships for those whose salaries are not keeping pace with the high-skill sectors. The June 2020 announcement that Japanese biopharmaceutical company AGC Biologics will invest $100 million in their new facility on the former AstraZeneca site in Boulder indicates that the region remains attractive to firms looking to do high-value manufacturing.(super: 48) The desirable location, quality of life and career opportunities will maintain the region’s luster for those who can afford it. Public investments to expand lower-cost housing options are necessary to allow more access to Boulder’s opportunities.

(image: boulder-table.jpg)

**San Francisco-Oakland-Hayward, California’s economy continued to advance at a strong pace just before COVID-19. **

The San Francisco metro area improved four places to fifth overall and second among large metropolitan areas in 2020. The San Francisco metro area was well-positioned to exploit the movement towards the digital economy. As a Superstar city, it has been attracting technical talent from across the globe. The broad region is second in the nation with 52 percent of the 25 and overpopulation with a bachelor’s degree or higher.(super: 49) One measure of San Francisco’s diversity is exhibited by 33 percent of its population being foreign-born. Because of restrictions on foreign travel and business activity to control the spread of COVID-19, the impact on leisure, restaurants, retail and other related sectors has been devastating. Short-term job momentum fell to 343rd in the nation, an employment decline of 11.2 percent.

The San Francisco metropolitan economy is huge, with 4.7 million people in 2019 and an employment base of 2.4 million, extending across the San Francisco Bay to Oakland and the East Bay. Despite the high cost of living in the Bay Area, San Francisco has the sixth-highest per capita personal income. San Francisco was sixth in the growth of average annual pay adjusted for inflation in 2019. The high-tech service sector has been fueling its growth over the last five years. It has excelled in mobile applications, social media, cloud-based software, internet publishing, gaming and digital media.(super: 50) Across our indicators, the San Francisco metro area was in the top 10 in three and had three others in the top 20.

More so than in Silicon Valley, young firms turning into unicorns fueled its recent growth. The majority of jobs created are in the tech area as startups scale into unicorns—Airbnb, Dropbox, Yelp and Zynga (market capitalization of at least $1 billion) developed in the city’s and region’s unique entrepreneurial ecosystem. Several more firms have joined the list of unicorns in 2020. However, software and digital tech giants such as Salesforce, Oracle, Facebook and Uber expanded at a prodigious rate in recent years, supporting overall job gains. High-wage jobs in the professional, scientific and technical services rose by 75 percent over the last decade, only exceeded by Austin among metropolitan areas with a population exceeding one million residents. Before the pandemic, unemployment fell below 3 percent in the metro area.

There is scant evidence that early-stage equity investors pulled back in 2019 or 2020. The San Francisco metro area has passed Silicon Valley in the availability of venture capital and angel investing. Venture capital investments in San Francisco totaled $24 billion in 2019, a decline of $7 billion from 2018. However, the 2018 figure was skewed by the $12.8 billion investment made by Altria Group into JUUL Labs—a manufacturer of electronic cigarettes. The number of mega-deals (above $100 million) in 2019 increased to 55 from 37 in 2018. The top megadeals in 2019 included Flexport, JUUL Labs, DoorDash, Chime and Uber Technologies.(super: 51) Further encouraging was San Francisco area based-firms received $301 million in angel investment in 2019, exceeding Silicon Valley firms. The initial public (IPO) window remained open in 2019, with 12 San Francisco area companies going public that employed over 50,000. Through September 2020, venture-backed IPOs had a valuation of $60.3 billion.(super: 52)

Between September 2019 and September 2020, the San Francisco metro area witnessed a 34.6 percent decline in leisure and hospitality employment. Food services and drinking places accounted for two-thirds of the loss in jobs and hotels and motels, along with arts, entertainment and recreation, accounted for the bulk of the remainder.(super: 53) TSA air passengers screened hit 2.1 million in February 2020, falling to 95,000 in April, and only recovered to 532,000 by September.(super: 54) Due to the ability to work remotely, employment at tech firms is down just 2.1 percent since February 2020 helping to minimize the broader economic impact. On the flip-side, lower-wage service employees are feeling pain as their enhanced unemployment insurance benefits ran out.

San Francisco’s technology startup scene is a unique one. The young firm knowledge intensity is second in the nation, with 35.6 percent of employees at young firms with a bachelor’s degree or above. The region’s ability to start, scaleup and take companies public at high valuations is remarkable. The urgent need to find therapeutic treatments and vaccines against COVID-19 has energized its thriving life science sector. The South San Francisco’s biomedical cluster is an important core of the region’s economy.

Genentech—the biotech pioneer—employs 8,800 in the region and was an early collaborator with 23andMe, a genetic testing leader for people desiring to know their ancestry.(super: 55) The research prowess of the University of California, San Francisco, is a critical component of the biomedical cluster. The East Bay has witnessed an expansion in biotech, with companies such as 10X Genomics calling the area home.

Tesla experienced a shutdown in production due to COVID-19 and announced it chose the Austin area for a new battery plant. Nevertheless, the company’s expansion into the East Bay is reshaping the area’s economic structure. Tesla achieved an important milestone by increasing production in four straight quarters.(super: 56) Tesla is adding jobs faster than any employer on the Oakland side of the Bay in Hawthorne, and employment stands slightly above 10,000. Tesla’s expansion is attracting automotive suppliers, tech support firms and automation and robotics investment.

The University of California, Berkeley, is an important member of the San Francisco metro area’s tech-focused economy. Not only is it an elite research university with many capable entrepreneurial students and faculty, but it provides much of the technical talent for the area’s firms. Since 2009, Berkeley undergraduates have founded 1,089 companies, including Cloudera, Zynga, Auris Surgical Robotics, Machine Zone and Sapphire Energy.(super: 57) In addition to innovation leadership, Berkeley is an anchor for diversity and community for the region. Berkeley employs 25,000 people, tying the University of California, San Francisco, for the metro’s top employer.

Given its dynamic entrepreneurial ecosystem, San Francisco’s economy should recover over the medium term. However, COVID-19 is reshaping where firms should locate their operations and the downsizing of needs for office and commercial space will hurt construction. Prior to COVID-19, congestion, high housing prices and transportation challenges caused the metro area to experience out-migration. During 2018 and 2019, 54,000 more people left the San Francisco metro area than moved in from other states. San Francisco had defied centrifugal forces by generating ever-higher levels of productivity from its innovation density and talent.(super: 58)Given the restrictions on reopening, local economists expect that the jobs lost won’t be recovered until the end of 2022.(super: 59)

Endnotes

- DeVol, Ross, Ratnatunga, Minoli, Shideler, Dave and Crews, Jonas. (2020, October), “Most Dynamic Micropolitans,” p.10, Heartland Forward, retrieved October 5, 2020. https://heartlandforward.org/most-dynamic-micropoli-tans-2020

- Crews, Jonas, DeVol, Ross, Florida, Richard, and Shideler, Dave. (2020, May 6). “Young Firms and Regional Economic Growth.” Heartland Forward, retrieved November 9, 2020. https://heartlandforward.org/young-firms-and-regional-economic-growth

- DeVol, Ross (2018, September), “How Do Research Universities Contribute to Regional Economies?,” Walton Family Foundation, retrieved May 9, 2019. https://8ce82b94a8c4fdc3ea6d-b1d233e3bc3cb10858bea65ff05e18f2.ssl.cf2.rackcdn.com/da/5d/7d56ea9a46de8d0ab5d0e5159ba5/new-research-universities-contribute .pdf

- DeVol, Ross, Ratnatunga, Minoli, Shideler, Dave and Crews, Jonas. (2020, October), “Most Dynamic Micropolitans,” p.10, Heartland Forward, retrieved October 5, 2020. https://heartlandforward.org/most-dynamic-micropoli-tans-2020

- Perryman, R. (2020, May 15). Keeping it Together!! Preserving the Permian Basin Energy Sector and the Odessa Economy through the COVID-19 and Related Oil Market Challenges, The Perryman Group. Retrieved Octo-ber 19, 2020, from https://www.perrymangroup.com/media/uploads/re-port/perryman-keeping-it-together-05-2020.pdf

- McEwen, M. (2019, February 5), “Perryman ‘optimistic about the area’,” retrieved October 18, 2020. https://www.mrt.com/business/article/Perry-man-optimistic-about-the-area-13592285 .php

- Matthews, C., (2019, March 1), “In This Oil Boom Town, Even a Barber Can Make $180,000,” Wall Street Journal, retrieved March 5, 2019 .https://www.wsj.com/articles/in-this-oil-boom-town-even-a-barber-can-make-180-000-1551436210?emailToken=64a99f2eaccbf5b3c1215721b2fd1b47gCq/7PR/atsD2aAbwwYYYWHbWHZigZGIWiWCvAepcRbhS5ma0O+Na6rnsVXa-jrIX61MWY/8bzX+PksDuBOk6n+1b22ePe40nQcbHSzr2DHB5CIFeLxy9ct-Vd4yb0u0dG&reflink=article_email_share&ns=prod/accounts-wsj.

- Golden Shovel Agency, M. (2019). Home. Retrieved October 14, 2020, from https://www.midlandtxedc.com/workforce/major-employers/?-cat=major employer

- Krauss, C. (2019, February 3), “How a ‘Monster’ Texas Oil Field Made the U.S. a Star in the World Market,” retrieved March 5, 2019. https://www.ny-times.com/2019/02/03/business/energy-environment/texas-permian-field-oil .html

- Golden Shovel Agency, M. (2019). Home. Retrieved October 18, 2020, from https://www.midlandtxedc.com/workforce/major-employers/?-cat=major employer

- Thurber, K. (2011, March 6), “Susie’s South Forty celebrates 20th year,” retrieved October 18, 2020. https://www.mrt.com/business/article/Susie-sSouth-Forty-celebrates-20th-year-7432573 .php#photo-10012099.

- UTPB. (2019). Roden Entrepreneurial Development center. Retrieved May 20, 2019, from https://www.utpb.edu/business/the-jan-and-ted-roden-cen-ter-forentrepreneurship/index.

- The Midland International Air & Space Port is Open for Business & FAA Approved, retrieved October 18, 2020 from https://www.midlandtxedc.com/spaceport-business-park

- Elliott, R. and Eaton, C. (October 20, 2020). “Pioneer Natural Resources to Buy Parsley Energy for $4.5 Billion,” Wall Street Journal, retrieved October 20, 2020, https://www.wsj.com/articles/pioneer-natural-resourc-es-to-buy-parsley-energy-for-4-5-billion-11603224139?st=b6r8gbq0g3wg-ga3&reflink=article_email_share.

- McEwen, M. (October 3, 2020). “Clean economy legislation could give boost to Permian carbon projects,” Midland Reporter-Telegraph, retrieved October 20, 2020, https://www.mrt.com/insider/article/Clean-economy-legislation-could-give-boost-to-15619026.php

- MDC Small Business Assistance Program, retrieved October 18, 2020, retrieved from https://www.midlandtxedc.com/business-and-economy/mdc-small-business-assistance-program

- Ratz, L., (2020, July), “San Jose-Sunnyvale-Santa Clara, California,” Moody’s Analytics, retrieved October 10, 2020. 18 Hancock, R. (2020, January), “2020 Silicon Valley Index,” p.3, retrieved October 20, 2020. https://jointventure.org/images/stories/pdf/index2020.pdf.

- Hancock, R. (2019, January), “2019 Silicon Valley Index,” p.31, retrieved March 7, 2019. `https://jointventure.org/download-the-2019-index21 Ratz, L. (2018, December 18), “San Jose-Sunnyvale-Santa Clara, California,” Moody’s Analytics, retrieved February 18, 2019.

- DeVol, R., Lee, J. and Ratnatunga, M. (2016, December), “2016 Best-Per-forming Cities: Where America’s jobs are created,” pp. 13, Milken Institute, retrieved October 18, 2020. https://assets1c.milkeninstitute.org/assets/Pub-lication/ResearchReport/PDF/BPC-2016-FINAL-WEB.pdf

- Hancock, R. (2019, January), “2019 Silicon Valley Index,” p.31, retrieved March 7, 2019. `https://jointventure.org/download-the-2019-index

- Ratz, L. (2018, December 18), “San Jose-Sunnyvale-Santa Clara, California,” Moody’s Analytics, retrieved February 18, 2019.

- Darrow, B. (2017, October 24), “Here’s Why Cisco Is Paying Nearly $2 Billion for BroadSoft,” Fortune, retrieved March 8, 2019. http://fortune.com/2017/10/24/cisco-buys-broadsoft/

- Du Sault, L. (2020, October 19), “For many Californians, the pandemic marks the end of “barely making it,” San Jose Mercury News, retrieved October 20, 2020. https://www.mercurynews.com/2020/10/19/for-many-californians-the-pandemic-marks-the-end-of-barely-making-it/.

- McEwen, M. (2019, February 06). Perryman ‘optimistic about the area’. Retrieved November 17, 2020, from https://www.mrt.com/business/article/Perryman-optimistic-about-the-area-13592285.php

- Joint Venture Silicon Valley, (2016, March), “2016 Silicon Valley Index: pp. 32-40, retrieved March 8, 2020 https://www.jointventure.org/images/sto-ries/pdf/index2016.pdf

- Hancock, R. (2020, January), “2020 Silicon Valley Index,” pp.46-47, retrieved October 18, 2020. https://jointventure.org/images/stories/pdf/index2020.pdf.

- Jackson, J., Lee, J., Lin, M. C.Y., & Ratnatunga, M. (2019). Best-Perform-ing Cities: Where America’s Jobs are Created and Sustained. Santa Monica: Milken Institute. Retrieved November 18, 2020, from https://milkeninstitute.org/reports/best-performing-cities-2020

- Trainer, D. (2018, July 03). Domo Richly Priced At Post-IPO Market Value. Retrieved November 18, 2020, from https://www.forbes.com/sites/greatspeculations/2018/07/03/domo-richly-priced-at-current-market-val-ue-after-ipo/.

- Provo City Corporation. (2019). Economic Development. Retrieved November 18, 2020. from https://www.provo.org/departments/economic-de-velopment